The personal & business tax rates & allowances in 2022/23.

The personal & business tax rates & allowances in 2022/23.

With the dawn of each new tax year, our clients are always keen to know the latest personal and business tax rates and allowances to ensure they are making the most of every opportunity, and have all the information they need to plan for the financial year ahead. This article covers some of the key tax rates and allowances for individuals and businesses for the tax year 2022/23, which started on the 6th April. Please note that the following information is specific to England and Wales only.

Personal tax rates for tax year 2022/23.

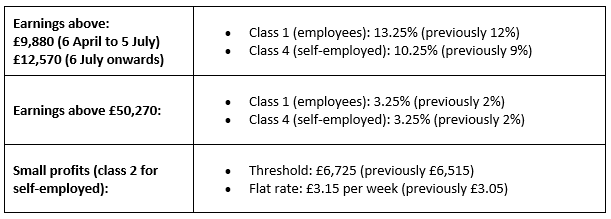

What are the National Insurance rates in the tax year 2022/23?

National Insurance contributions (NICs) have risen by 1.25 percentage points. The government says this money will be spent on the NHS, health and social care.

The National Insurance threshold will rise by £3,000 in July 2022, meaning people must earn £12,570 before paying income tax or National Insurance. The upper earnings threshold, however, has been frozen at £50,270. Employees pay a lower rate of National Insurance above this point.

The NIC rates for the 2022/23 tax year are as follows:

NIC rates for the 2022/23 tax year.

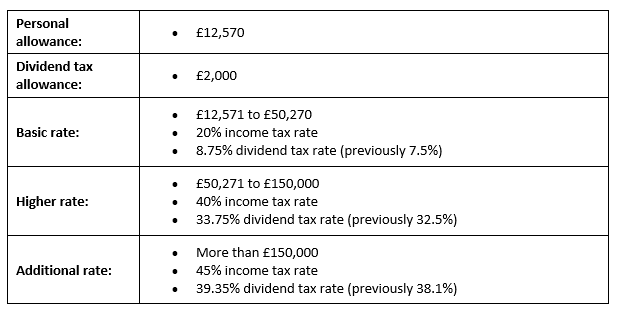

What are the Income & Dividend tax bands and rates in the tax year 2022/23?

A significant change to come sees a cut to the basic rate of income tax rate from 20% to 19%, however this will not happen until 2024. This will be the first cut to the basic rate of income tax for 16 years.

The personal allowance and income/dividend tax thresholds have been frozen until April 2026.

Rates of dividend tax have increased by 1.25 percentage points. The dividend allowance remains unchanged at £2,000.

The income and dividend tax bands and rates for the 2022/23 tax year are as follows:

Income and dividend tax bands and rates for the 2022/23 tax year.

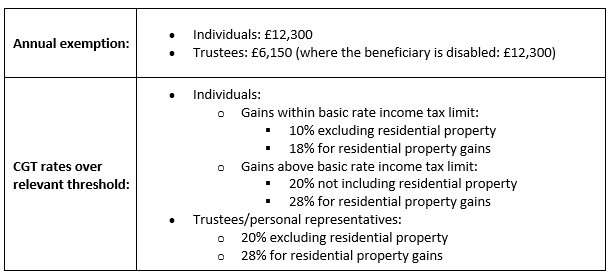

What are the Capital Gains Tax (CGT) & Inheritance Tax (IHT) rates and thresholds in the tax year 2022/23?

Two reporting rules were brought in prior to the new tax year that are worth noting here:

CGT on sale of a property. Previously, there had been a window of just 30 days for taxpayers to report the gain and pay the tax owed. From the Budget on 27 October 2021, this was immediately increased to 60 days.

IHT in respect of death on or after 1 January 2022. There are new rules about whether or not an estate can be classed as an ‘excepted estate’. Estates classed as being ‘excepted’ may not require heirs to report the estate’s value, as long as there is no IHT to pay.

An estate is usually an excepted estate if any of the following apply:

Its value is below the current Inheritance Tax threshold of £325,000

The estate is worth £650,000 or less and any unused threshold is being transferred from a spouse or civil partner who died first

The deceased left everything to a spouse or civil partner living in the UK or to a qualifying charity and the estate is worth less than £3 million

The deceased was living permanently outside the UK (a ‘foreign domiciliary’) when they died, and the value of their UK assets is under £150,000

To qualify, none of the reasons stated on gov.uk under ‘when you need to send full details of the estate’s value even if no tax is due’ can apply.

Further details can be found on the government website under How to value an estate for Inheritance Tax and report its value.

CGT and IHT thresholds and rates remain unchanged.

The CGT thresholds and rates for the 2022/23 tax year are as follows:

CGT thresholds and rates for the 2022/23 tax year.

The IHT thresholds and rates for the 2022/23 tax year are as follows:

IHT thresholds and rates for the 2022/23 tax year.

What are the Pensions Lifetime Allowance (LTA) & Annual Allowance (AA) in the tax year 2022/23?

All thresholds remain unchanged.

The LTA and AA thresholds for the 2022/23 tax year are as follows:

LTA and AA thresholds for the 2022/23 tax year.

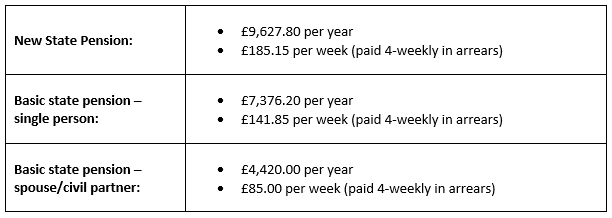

What is the State Pension in the 2022/23 tax year?

If you reached State Pension age before 6 April 2016, you will receive the Basic State Pension. Those reaching State Pension age after this date will be eligible for the New State Pension.

The increase to both State Pensions was set by the UK government at 3.1% from 6 April, which reflected CPI in September 2021. This is the first time the ‘triple lock’ (which guarantees an increase in the State Pensions of the highest of average earnings, CPI and 2.5%) has not been honoured since it was introduced in 2010.

The State Pension amounts for the 2022/23 tax year are as follows:

State Pension amounts for the 2022/23 tax year.

Please note, you will not receive your new State Pension automatically - you have to claim it. You should receive a letter no later than 2 months before you reach State Pension age, telling you what to do. However, if you are within 4 months of reaching your State Pension age you can make a claim online via the government website.

Business tax rates for tax year 2022/23.

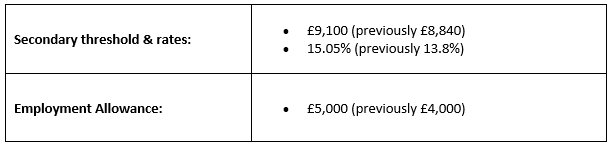

What are the National Insurance rates & the Employee Allowance in the tax year 2022/23?

National Insurance contributions (NICs) have risen by 1.25 percentage points. The government says this money will be spent on the NHS, health and social care.

The Employment Allowance (a relief that allows smaller businesses to reduce their employer NIC bills each year), has increased from £4,000 to £5,000.

The NIC rates and employment allowance for the 2022/23 tax year are as follows:

Employer NIC rates and employment allowance for the 2022/23 tax year.

What is the Minimum Wage in the tax year 2022/23?

There have been increases in the minimum wages following recommendations made by the Low Pay Commission in October 2021.

The minimum and living wage for the 2022/23 tax year are as follows:

The minimum and living wage for the 2022/23 tax year.

What Business Rates schemes are available in the 2022/23 tax year?

The 2022/23 Retail, Hospitality and Leisure Business Rates scheme provides eligible, occupied, retail, hospitality, and leisure properties with a 50% relief, up to a cash cap limit of £110,000 per business.

There are no business rates due on a range of green technology used to decarbonise buildings, including solar panels and batteries, while eligible heat networks will also receive 100% relief.

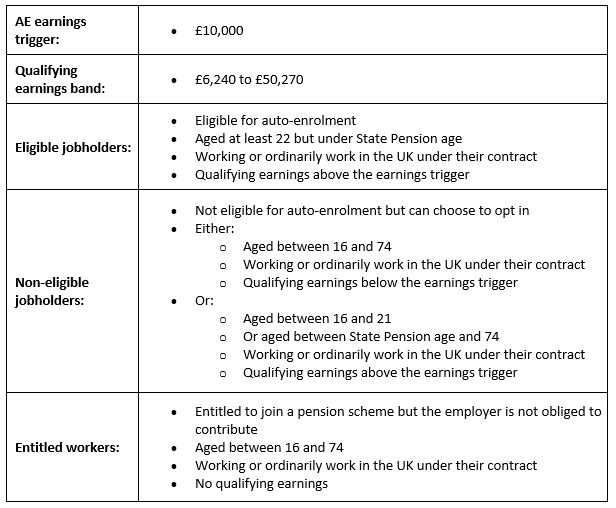

What are the criteria for Auto-Enrolment (AE) in the 2022/23 tax year?

Under auto-enrolment rules, employers must enrol all workers in a workplace pension that meets age and earnings criteria.

There are no changes to the thresholds/criteria this year.

The AE criteria for the 2022/23 tax year is as follows:

AE criteria for the 2022/23 tax year.

What are the VAT rules in the 2022/23 tax year?

All businesses registered for VAT must follow the Making Tax Digital (MTD) for VAT rules.

This includes businesses that voluntarily registered for VAT and were left out in the initial April 2019 launch of Making Tax Digital for VAT because they were below the £85,000 threshold.

The VAT rates have not changed, with the exception of the ending of coronavirus relief measures aimed at the hospitality sector. The 20% rate resumed from 1 April 2022.

The VAT threshold, which determines whether a person must be registered for MTD, remains frozen at £85,000 until 1 April 2024.

What are the Corporation Tax rates in the 2022/23 tax year?

There is no increase in corporation tax for the 2022/23 tax year – it remains at 19%.

However, it changes on 1 April 2023, when corporation tax rises from 19% to 25% on profits over what will be referred to as an Upper Profits Threshold of £250,000. This will be the first rise in corporation tax since 1974.

The Small Profits Rate will apply to profits under £50,000, where the rate will remain at 19% as of April 2023.

For those with profits between £50,000 and £250,000, it may be possible to claim some marginal tax relief to reduce the 25% rate.

What Capital Allowances are available in the 2022/23 tax year?

A super-deduction capital allowance can be used until 31 March 2023. This is set at 130% and means companies investing in qualifying new plant and machinery assets can claim back the cost as a first-year capital allowance, plus 30% on top of that. The goal is to encourage firms to invest and therefore grow.

There is a further capital allowance measure for investing companies that benefit from a 50% first-year allowance for qualifying special rate (including long life) assets.

What changes have been made to the IR35 regulations in the 2022/23 tax year?

HMRC has ended its one-year moratorium on penalties for private sector hiring businesses who accidentally breach the new IR35 off-payroll working rules.

IR35 rules (imposed on public sector organisations in 2017 and extended to private sector companies and charities from 6 April 2021) are designed to combat tax avoidance through ‘disguised employment’, a practice whereby employees are incorrectly classified as contractors, allowing clients and contractors to pay less tax and National Insurance Contributions.

HMRC has improved its check employment status for tax (CEST) online tool to help hirers conduct their status determinations.

Conclusion.

As you can see, there have been a handful of changes changes made to the business and personal tax rates and allowances for the 2022/23 tax year. Not all of it will apply to everyone, however it’s important to stay updated to help with planning your finances this year.

What’s next?

If you need help or advice on your personal or business finances, you can get in touch with one of our advisors for independent financial advice. We offer a free initial consultation and although we are based in Tunbridge Wells, we advise clients across the UK.

Don’t forget, this article offers information about tax rates and allowances and should not be taken as personal advice. Remember that investments and pensions can go up and down in value, so you could get back less than you put in. Tax rules can change and the benefits depend on individual circumstances.