How much do I need in my pension pots to retire?

How much do I need in my pension pots to retire?

[*This article was last updated 26/01/26.]Introduction.

We all hope for a comfortable retirement. To make sense of any retirement planning exercise, and to get the most from your pension savings, it’s important to have a clear target to work towards.

Once you have an idea of how much you may need in your pension pots, you can begin to fine-tune your saving strategy, set realistic expectations, and understand the level of retirement income you might be able to generate when you stop working. The question most people ask at this stage is simple, but important: how much do I need in my pension pots to retire?

To help you get a quick answer, we’ve built a basic pension pot calculator that estimates how much capital may be required to support a given level of income in retirement. If you’re short on time, you can jump straight to the calculator below, or read on for a deeper explanation of the assumptions, trade-offs, and variables involved.

At a glance

Q: How much do I need in my pension pots to retire?

A: As a broad guide, people aiming for a moderate retirement today often target pension savings in the region of £900k – £1.2m for a single person or £1.2m – £1.6m for a couple.

These figures assume a long-term drawdown approach of around 4%, with retirement income coming from a mix of sources - some taxed at basic rate and some drawn tax-free, such as pension cash or ISAs - and are calculated independently of the State Pension.

The sums required for a modest retirement lifestyle could be significantly lower, while a comfortable or wealthy retirement lifestyle would typically require substantially more. The right target depends on how you want to live in retirement, not just the headline numbers.

Note that the full UK State Pension currently provides around £12,000 per year, which is broadly equivalent to around £300,000 of pension capital at a 4% withdrawal rate. For many people, this means the private pension pot required may be lower, depending on eligibility, timing and future policy.

However, given the long-term cost of providing the State Pension and ongoing debate around the triple lock, many people choose to plan their retirement without relying on it. Any State Pension entitlement can then be treated as an additional layer of security, rather than something your retirement depends on.

Making sense of the numbers.

This article explains in detail how these figures are calculated, the assumptions behind them, and how different lifestyle choices and income sources can materially change the outcome.

If you’d like to sense-check these figures against your own circumstances, a short conversation with an independent adviser can help you understand what’s realistic, what’s flexible, and what trade-offs may be involved. Your initial consultation is free and comes with no obligation to proceed.

For a deeper explanation of how these figures are calculated, read on below or use the calculator to estimate your retirement income.

What is a pension?

First of all, we need to understand what a pension is. Typically, a pension falls into one of three categories:

State Pension: A regular pension income provided by the UK Government once you reach state pension age and have a sufficient National Insurance record.

Private Pension (also known as a Personal Pension): A type of 'investment wrapper' that is designed to pay out once you reach retirement age (known as pension drawdown or income drawdown). In many circumstances, personal pensions offer a degree of tax relief while you are working.

Workplace Pension: A type of pension scheme that is set up by your employer whereby pension contributions are deducted from your wages and your employer makes an additional pension contribution as an employee benefit. Workplace pension schemes are usually either a 'defined contribution pension' or a 'defined benefit pension'.

Your total retirement income will consist of the income from a state pension, private pension, and workplace pension combined, plus any additional income you may have from other investments such as rental properties, ISAs, and shares.

To take a more detailed look at the different types of pensions, find out what a pension scheme is and understand pension tax relief on pensions, you can read our dedicated article that explains the basics of pensions.

What is a pension pot?

The term pension pot is commonly used to describe the total value of your pension savings. This may refer to a single combined figure or to the balances held across multiple pension accounts. For example, you might say:

“I have £430,000 in my pension pot.”

Or:

“I have £245,000 in this pension pot, £136,000 in that pension pot, and £49,000 in another pension pot.”

Both descriptions are perfectly valid and would be understood by any financial professional.

You may also hear the term pension fund used interchangeably. While this is often used casually to mean pension savings, it can also refer more specifically to the pooled investments managed by a pension provider on behalf of many individuals.

Why people have multiple pension pots.

It’s very common to hold more than one pension pot. Over the course of a working life, you may accumulate:

Several workplace pensions from different employers.

One or more personal pensions or SIPPs (Self-Invested Personal Pensions).

As a result, many people reach later life with a collection of pension pots rather than a single account.

If you’re unsure whether you’ve tracked down all your pensions (or think you may have a lost pension) the gov.uk pension tracing service can help you locate them.

Pensions are not the only source of retirement income.

While pensions are often the primary source of retirement income, they are rarely the only asset used to support spending in retirement.

Many people also rely on a wider pool of assets, such as:

ISAs and other tax-efficient investments.

Cash savings.

General investment accounts.

Property or rental income.

Business assets or other capital.

These assets are often used alongside pensions to:

Reduce the amount of taxable pension income drawn each year.

Provide flexibility in how and when income is taken.

Improve tax efficiency in retirement.

For this reason, when people talk about “how much they need to retire”, they are often really referring to the total pool of assets available to generate income, not just the value of their pension pots in isolation.

Throughout this article, we focus on pension pots because they are central to retirement planning and benefit from significant tax advantages - but in practice, effective retirement planning looks at all assets working together.

How much income do I need in retirement?

The different retirement lifestyles.

The Department for Work and Pensions (DWP) has researched the level of income people will need in retirement (retirement income), and, as a general rule, the more you earn whilst working, the more income you will need in retirement. Equally, the less money you earn whilst working, the higher percentage of that income you will need in retirement as there are some basic living costs to be met to maintain retirement living standards.

Their report also highlighted three different lifestyles that one can adopt during retirement: basic, comfortable, and wealthy. Furthermore, it was proposed that there is a hierarchy of needs to be met around security, independence, and choice.

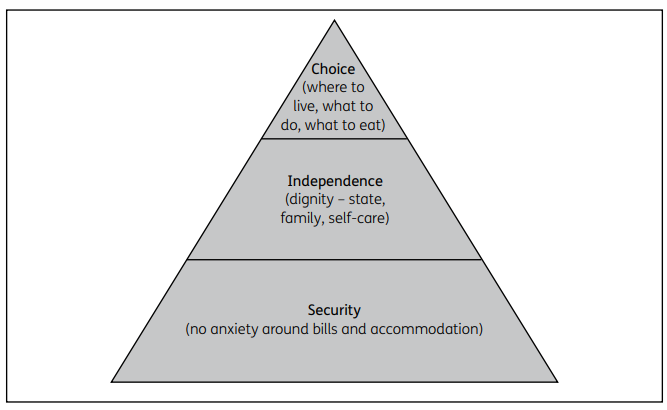

The hierarchy of needs in retirement.

Everyone in retirement needs security of accommodation, food and their bills paid as a baseline, alongside the ability to deal with financial emergencies, such as a boiler breakdown. The next tier of importance is for retirees to have independent living without outside assistance from the state, friends or family. Finally, choice is a luxury that enables those in retirement to enhance their lives with things like holidays, leisure activities and the quality of their accommodation.

You can quickly start to understand how the three lifestyles of basic, comfortable and wealthy will impact a retiree’s ability to achieve the hierarchy of needs. For example, a basic lifestyle may only offer the baseline securities; however, a spike in energy prices or the refrigerator packing up will likely introduce a degree of financial anxiety. They may also rely on the state or family to cover their income or provide care.

Conversely, those in a comfortable position can cover the basics and have independence and a degree of choice around what they do in their leisure time. Whereas those that fall into the wealthy lifestyle will have total security of accommodation, be able to deal with life’s curveballs, not be reliant on anyone else, able to choose the type of house they live in and the frequency they take holidays and such. Most respondents in the research tended to be drawn to the comfortable lifestyle and wanted to distance themselves from both the poverty of the basic lifestyle and the extravagance of the wealthy lifestyle, although this is, of course, a personal preference.

It’s clear then that everyone wants to have secure accommodation, a financial buffer, independence and at least some degree of leisure spending and choice in retirement. For this reason, the category of comfortable can be further refined into:

A marginally comfortable retirement.

A moderately comfortable retirement.

A very comfortable retirement.

Ask yourself: What kind of lifestyle do you have now while working, and what are your lifestyle expectations during retirement?

Finding this useful?

Once a month, we send our latest articles on pensions, investments, mortgages, protection, estate planning and more - along with a couple you might have missed. Practical reading for anyone taking their finances seriously.

Join our readers →Putting your retirement lifestyle options into numbers.

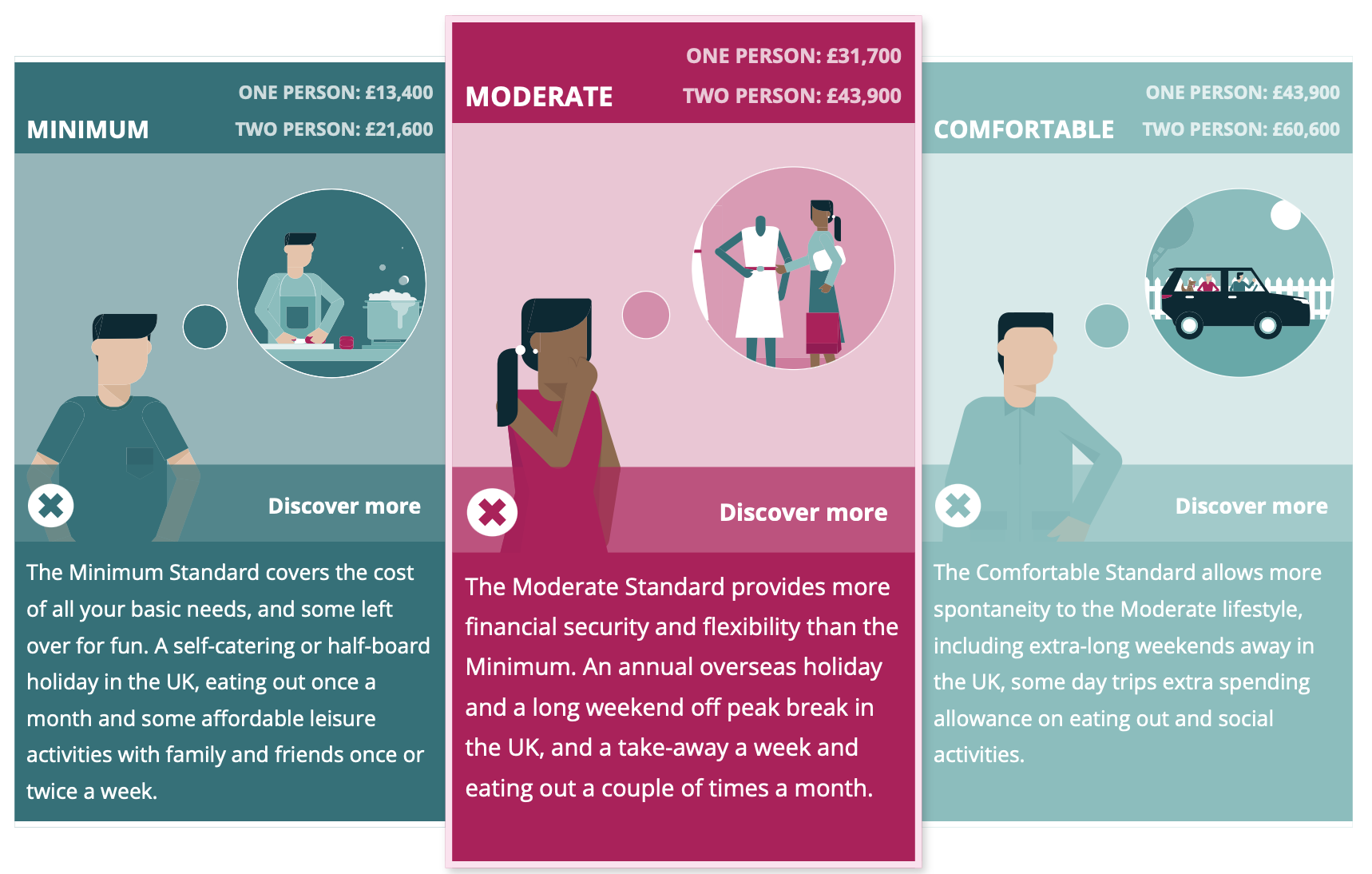

The Pensions and Lifetime Savings Association (PLSA) has also conducted detailed research into retirement living standards, and they have launched a matrix of lifestyles and the amount of income you need to generate in retirement to achieve those particular lifestyles. Their lifestyle categories broadly align with the three varieties of the ‘comfortable retirement’ category in the DWP research.

Minimum = A marginally comfortable retirement.

Moderate = A moderately comfortable retirement.

Comfortable = A very comfortable retirement.

However, the PLSA income estimates exclude the equivalent of a basic lifestyle at one end of the spectrum and a wealthy lifestyle at the other.

How much income do I need in retirement (2026)?

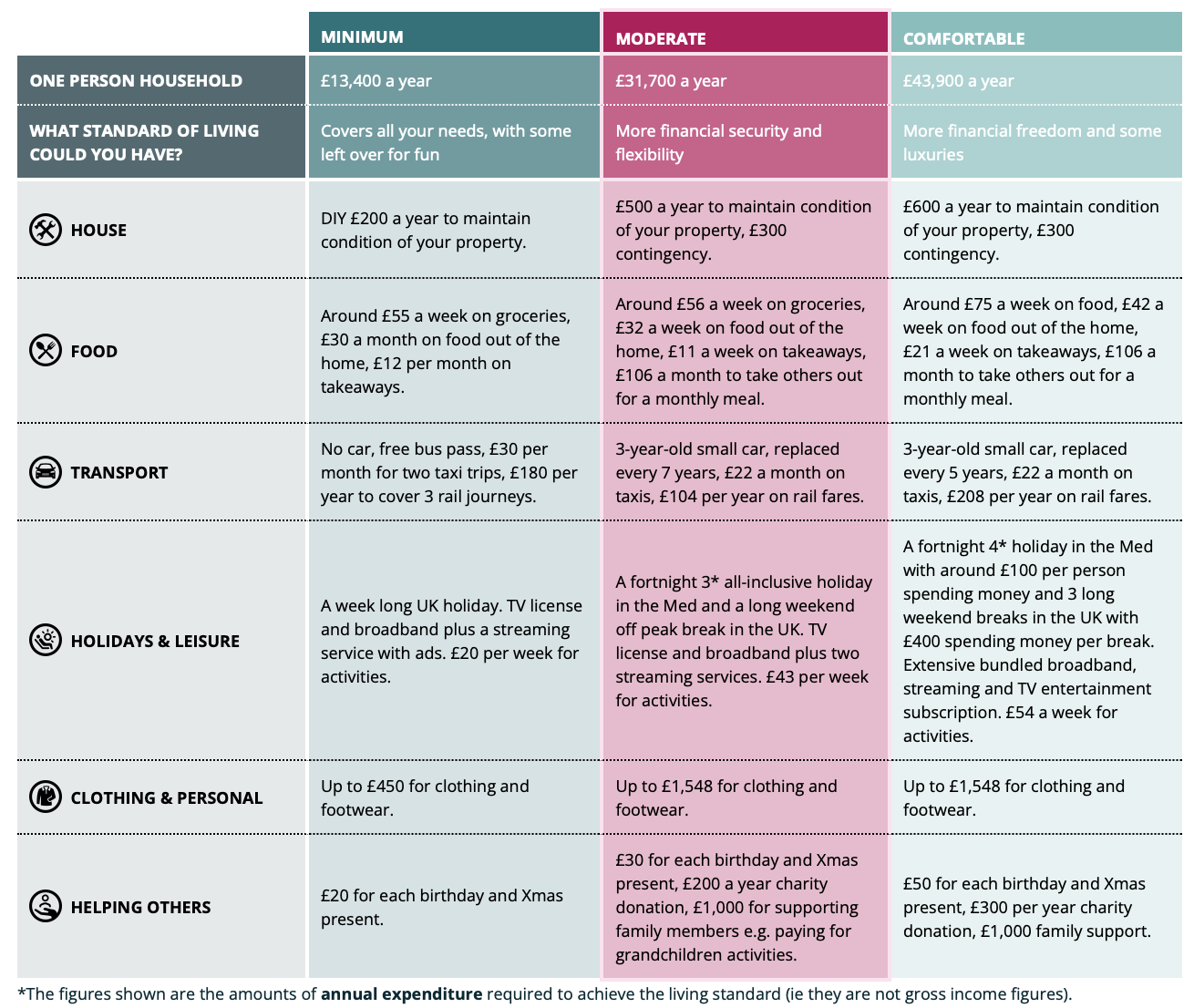

As you can see from the table above, the amount of income needed in retirement ranges from about £13,400 for a single person to enjoy a ‘minimum lifestyle’ to over £60,000 and above for a couple to enjoy a comfortable lifestyle. The PLSA even goes on to describe how these income requirements breakdown, for both individuals and couples.

Standard of living in retirement (singles 2026).

Standard of living in retirement (couples 2026).

Everyone's income needs during retirement will vary, according to individual circumstances - you or someone you care for may have complex health needs or perhaps you plan to travel extensively when you retire, for example. For most people, though, their living expenses will reduce once they retire as the mortgage will have been paid off, there are no more commuting costs (you could go down to one car), and you are no longer making pension and retirement savings. Your lifestyle ambitions really depend on how much you can save and invest while working.

Note that these figures do not account for taxation, the provision of a state pension income (depending on your circumstances) or the other benefits or tax credits you may be entitled to claim. The reason for this approach is that with an ageing population and consistent delays to the age by which you can claim the state pension, we believe it's best to prepare a retirement fund that is independent of outside assistance as there is no guarantee it will be available when you need it.

How much do I need in my pension pot to provide an income in retirement if I am single?

According to the Pensions and Lifetime Savings Association (PLSA), a single person aiming for a moderate standard of living in retirement will need an income of around £31,700 per year after tax.

As a broad guide, providing this level of income over the long term typically requires a pension and retirement savings pot in the region of £900,000 - £1.2m, assuming a sustainable withdrawal rate of around 4%.

The size of the pot required depends heavily on how the income is structured. Where retirement income is drawn entirely from a taxable pension, a larger fund is usually needed. However, many people reduce the amount of tax paid by combining:

Pension drawdown within the personal allowance,

The 25% tax-free lump sum, and/or

Income from ISAs or other tax-free investments.

In more tax-efficient scenarios, the effective tax rate on retirement income can be low, which may bring the required pot closer to the lower end of the range. Less tax-efficient or more cautious strategies tend to sit toward the upper end.

While £31,700 is mathematically equivalent to around 4% of £790,000, real-world retirement planning usually allows for tax, flexibility, inflation and uncertainty, which is why many people target a higher figure.

These estimates also assume planning largely independently of the State Pension, with any entitlement treated as an additional layer of security rather than something the plan relies on.

How much do I need in my pension pot to provide income for a couple in retirement?

According to the Pensions and Lifetime Savings Association (PLSA), a couple aiming for a moderate standard of living in retirement will need an income of around £43,900 per year after tax.

As a broad guide, providing this level of income over the long term typically requires a combined pension and retirement savings pot in the region of £1.2m–£1.6m, assuming a sustainable withdrawal rate of around 4%.

The size of the pot required depends on how retirement income is structured. Where income is drawn primarily from taxable pensions, a larger fund is generally needed. However, couples often have greater flexibility to manage tax efficiently by combining:

Pension withdrawals spread across two personal allowances,

Tax-free pension cash, and

Income from ISAs or other tax-free investments.

In more tax-efficient scenarios, the effective tax rate on retirement income can be relatively low, which may bring the required pot closer to the lower end of the range. Less tax-efficient or more conservative strategies tend to sit toward the upper end.

While £43,900 is mathematically equivalent to around 4% of £1.10m, real-world retirement planning usually allows for tax, flexibility, inflation and uncertainty, which is why many people target a higher figure.

As with individual planning, these estimates assume building a plan largely independently of the State Pension, with any entitlement treated as an additional layer of security rather than something the plan depends on.

What size pension pot do I need to provide a wealthy lifestyle in retirement?

The Pensions and Lifetime Savings Association (PLSA) lifestyle figures focus on minimum, moderate and comfortable standards of living and do not extend to a wealthy or high-spending retirement.

If you are accustomed to a high income while working, your retirement income needs may be significantly higher than £60,000 per year after tax. In these circumstances, the level of pension and retirement savings required increases materially.

As a broad guide, generating an income of around £100,000 per year on a sustainable basis could require a total retirement fund in excess of £2.5m, assuming a long-term withdrawal rate of around 4%. Higher income targets or more cautious withdrawal assumptions would require a larger fund.

As with the other examples in this article, these figures are intended to support planning independently of the State Pension, which is subject to ongoing policy and affordability pressures. Any entitlement can then be treated as an additional layer of security rather than something a retirement plan depends on.

How do my investments change when I retire?

While you are working and contributing to your retirement savings, investment strategies are typically focused on capital growth. Income and gains are reinvested to benefit from compounding, with less emphasis on short-term volatility.

As you approach retirement, and particularly once you start drawing income, that focus often shifts. Instead of maximising growth alone, the emphasis moves toward generating sustainable income, managing risk, and preserving capital over what may be a long retirement.

At this stage, there is no single “right” approach. The strategy that makes sense depends on your income needs, attitude to risk, overall wealth, and how much flexibility you want.

Common approaches in retirement.

Depending on your circumstances, you may choose one or a combination of the following:

Reducing investment risk.

Some people prioritise certainty and choose to reduce exposure to market volatility. This may involve allocating part of their pension or assets to lower-risk investments or securing a guaranteed income, such as an annuity. In doing so, you trade potential growth for greater income security.

Maintaining exposure for income and growth.

Others continue to accept a degree of investment risk, drawing income from portfolios invested in growth and income-producing assets. This approach offers flexibility and the potential for higher income, but returns, and income, are not guaranteed and can fluctuate over time.

Using a blended or layered strategy.

Those with larger or more complex asset bases often adopt a mixed approach. This might include securing a base level of guaranteed income to cover essential spending, alongside invested assets to provide discretionary income, flexibility, and the potential for continued growth or legacy planning.

Risk, longevity and flexibility.

Your chosen approach will directly affect:

How resilient your income is during market downturns.

The risk of running out of money later in life.

How much flexibility you retain to adapt to changing needs.

Simply drawing down from a pension, even at a commonly used rate such as 4%, without any form of guaranteed income introduces longevity risk, particularly if investment returns are weaker than expected.

For this reason, investment decisions around retirement are best considered well in advance, and reviewed regularly as circumstances change.

What else do I need to consider?

Retirement planning is rarely static. At or around retirement, you may also need to account for:

Taking a lump sum to repay a mortgage, fund major purchases or support family.

The impact of income tax and the use of available allowances.

Future care needs and later-life costs.

How much control you want to retain over your investments.

Whether leaving money to others is a priority.

Each of these factors can materially affect how much income you can safely take and how your assets should be structured.

Because these decisions interact - investment risk, tax, income timing and longevity - many people choose to work with a qualified financial adviser to help build and maintain a retirement strategy that remains robust over time.

Turning your retirement savings into a plan.

Knowing how much you may need in retirement is only part of the picture. How your income is generated, how tax is managed, and how risk is controlled over time can make a material difference to outcomes.

A short conversation with an independent financial adviser can help you sense-check your assumptions, understand your options, and build a strategy that reflects your priorities, both now and in later life.

A simple starting point (and its limitations).

With all of the above in mind, the question of “how much is enough” doesn’t have a single answer. Your target depends on how your income is generated, how it’s taxed, and how long it needs to last.

That said, many people find it helpful to start with a simple rule of thumb.

A commonly used starting point is a 4% long-term withdrawal rate. Using this approach, you divide your desired annual retirement income by four and multiply the result by 100 to estimate the capital required.

Indicative Capital Target = ((Annual Income Target ÷ 4) × 100)

This calculation is not a plan. It does not account for:

Taxation across different income sources

Use of tax-free cash or ISAs

State Pension entitlement

Changes in spending over time

Longevity or care needs

It is simply a way to sense-check the scale of savings required before moving into more detailed modelling.

The basic pension pot calculator below does this for you and allows you to explore different withdrawal rates as a starting point.

Basic Pension Pot Calculator.

Our Basic Pension Pot Calculator is a simple way to sense-check the scale of pension savings required to support a chosen retirement income. It is designed to provide high-level estimates only, before moving into more detailed modelling that takes account of tax, investment structure and changing circumstances.

How to use the basic pension pot calculator.

Enter your target income: This can be the income you would like to receive per month or per year in retirement.

Select the income frequency: Choose whether your income figure is monthly or annual. Annual is selected by default.

Choose a withdrawal rate: Select the percentage you plan to withdraw from your pension each year. You can choose 3%, 4% or 5%, with 4% used as a commonly referenced long-term guide.

View your estimate: The calculator will estimate the total pension pot required to support your chosen income at the selected withdrawal rate.

Important to understand.

This calculator does not account for tax, investment wrappers (such as ISAs), State Pension income, or other assets. It is intended as a high-level sense-check and typically reflects the lower end of the capital required to support a target income before more detailed planning.

Actual retirement income is usually drawn from multiple sources, often structured to minimise tax.

Withdrawal rates are illustrative only and may not be sustainable in all market conditions.

This tool is intended to help you sense-check affordability and scale, not to replace personalised retirement planning.

Basic Pension Pot Calculator

Understanding your results.

The calculator shows your target income, followed by the indicative level of capital required based on the withdrawal rate selected. The figure is designed to help you understand the scale of savings involved, rather than provide a precise or personalised retirement plan.

Every retirement is different. Tax, investment structure, timing of withdrawals, State Pension entitlement, and use of other assets can all materially change the outcome.

What to do next?

If you’d like to sense-check these results against your wider financial position, a short conversation with an independent financial adviser can help you understand what’s realistic, what’s flexible, and where the key trade-offs sit. Your initial consultation is free, confidential, and comes with no obligation to proceed.

Pension savings FAQs.

Is a £500,000 pension pot enough to retire?

A £500,000 pension pot could potentially support an income in the region of £20,000 per year (around £1,650 per month) using a long-term withdrawal rate of approximately 4%.

Whether this is “enough” depends entirely on your circumstances. Factors such as tax, investment performance, charges, life expectancy, State Pension entitlement, and whether income is supplemented by ISAs or other assets will all affect how long the money lasts and the standard of living it can support.

For some people, £500,000 may be sufficient as part of a broader retirement plan. For others, it may fall short.

How much pension pot do I need for £1,000 per month income?

An income of £1,000 per month equates to £12,000 per year. Using a 4% withdrawal rate as a broad guide, this would suggest a pension pot of around £300,000. In practice, the required figure may be higher or lower depending on tax treatment, use of tax-free cash, State Pension income, and whether other assets (such as ISAs) are contributing to retirement income.

How much pension pot do I need for £2,000 per month income?

£2,000 per month is £24,000 per year. At a 4% withdrawal rate, this implies a pension pot of approximately £600,000. This figure assumes the income is taken primarily from pension savings and does not account for tax efficiency, other income sources, or changes in withdrawal levels over time.

How much pension pot do I need for £3,000 per month income?

£3,000 per month is £36,000 per year. Using the same methodology, a pension pot in the region of £900,000 may be required. However, many retirees combine pension income with ISAs, cash savings, or part-time work, which can materially reduce the amount that needs to be drawn from pensions alone.

How much pension pot do I need for £4,000 per month income?

An income of £4,000 per month (£48,000 per year) would typically require a pension pot of around £1.2 million at a 4% withdrawal rate. At this level, tax planning and the sequencing of withdrawals become increasingly important, as small changes in structure can significantly affect net income and sustainability.

How much pension pot do I need for £5,000 per month income?

£5,000 per month equates to £60,000 per year. As a broad guide, this would suggest pension savings of around £1.5 million. In practice, higher-income retirees often rely on a mix of pension drawdown, tax-free cash, ISAs, and other investments rather than drawing the full amount from pensions alone.

A note on these figures.

All of the examples above are illustrative only. They assume a steady withdrawal rate and do not fully reflect tax, investment volatility, changes in spending over time, or the role of other assets.

They are best used to sense-check the scale of savings required, before moving into more detailed retirement modelling and advice.

If you’d like to understand how these figures apply to your own situation, a conversation with an independent adviser can help bring clarity around what’s achievable and how best to structure your retirement income.

What’s next?

If you’d like to move from broad guidance to your own numbers, the next step is to speak to one of our Independent Financial Advisers.

A free initial consultation is designed to answer your questions, sense-check your thinking, and help you understand how different income sources may fit together, including pensions, ISAs, tax allowances and other assets, based on your circumstances.

If you decide to proceed beyond this initial conversation, our paid advice process includes detailed retirement cash-flow modelling. This looks at how your income and capital may evolve under different scenarios, not just at retirement, but throughout later life, helping you make informed long-term decisions.

Based in Tunbridge Wells, we advise clients across the UK. Your initial consultation is free, confidential, and comes with no obligation to proceed.

This article provides general information about pensions and investing and should not be taken as personal financial advice. Investments can go down as well as up, and you may get back less than you invest. Tax rules can change, and benefits depend on individual circumstances.