Fact Check: Residential property offers huge capital growth opportunities.

*This article was first published in November 2020 and last updated Feb 2022.

Over the years I’m sure we’ve all heard people say that property is the best investment, the stock market and pensions are a con and that buy to let wins every investment argument. This article aims to shed some light on real-world residential investment and how the rosy picture of capital growth is heavily affected by a heated, pre-global financial crises market.

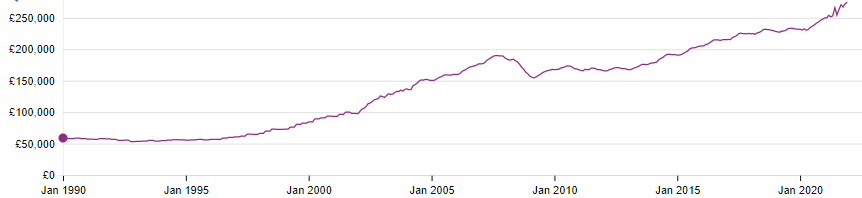

Property prices over the last 22 years.

National house prices are largely determined by individual buyers rather than investors, although in any given locality, buy to let investors can push up local property prices to levels that are unaffordable to locals. As such, we will use the national average prices of all properties for comparison, rather than drilling down to property types or locations.

To kick-off, over the last 22 years, the average property value has risen by £189,000 or 222% from £85,000 in 1990 to £274,000 in 2022, giving an average annual growth of £8,590 or 10.1%. However, these returns are heavily influenced by the rapid growth seen in the first decade, followed by significantly lower growth in the second decade and can be misleading.

To set the scene, house price growth really kicked off in the late 1990s. By 2000, the average price of a house in the UK was still only £85,000 and, over the next 8 years, this rose by an astonishing £100,000 to £185,000 in 2008, giving an 8-year return of 117% and an average annual growth of £12,500 or 14.7%.

However, in 2008 the party ended during the global financial crisis and just one year later in 2009, the average house price had dropped by £28,000 or 15% to £157,000. Over the ten years that followed, the average price increased by a more measured £71,000 or 45% to £228,000 in 2019, giving an average annual growth of £7,100 or 4.5%. More specifically, over the 5 years, from Jan 2015 to Jan 2020, the average property grew from £190,000 to £231,000 in 2020, an increase of 21% and an average annual growth of 4.3%.

As the UK started to emerge from the first-wave of Covid in 2020 and people decided they needed more space at home, the property market has seen some tremendous growth. In January 2020, the average house price was £231,000 which increased to £274,000 in December 2021. This is an increase of £43,000 or 18.6%.

How does property compare to the stock market?

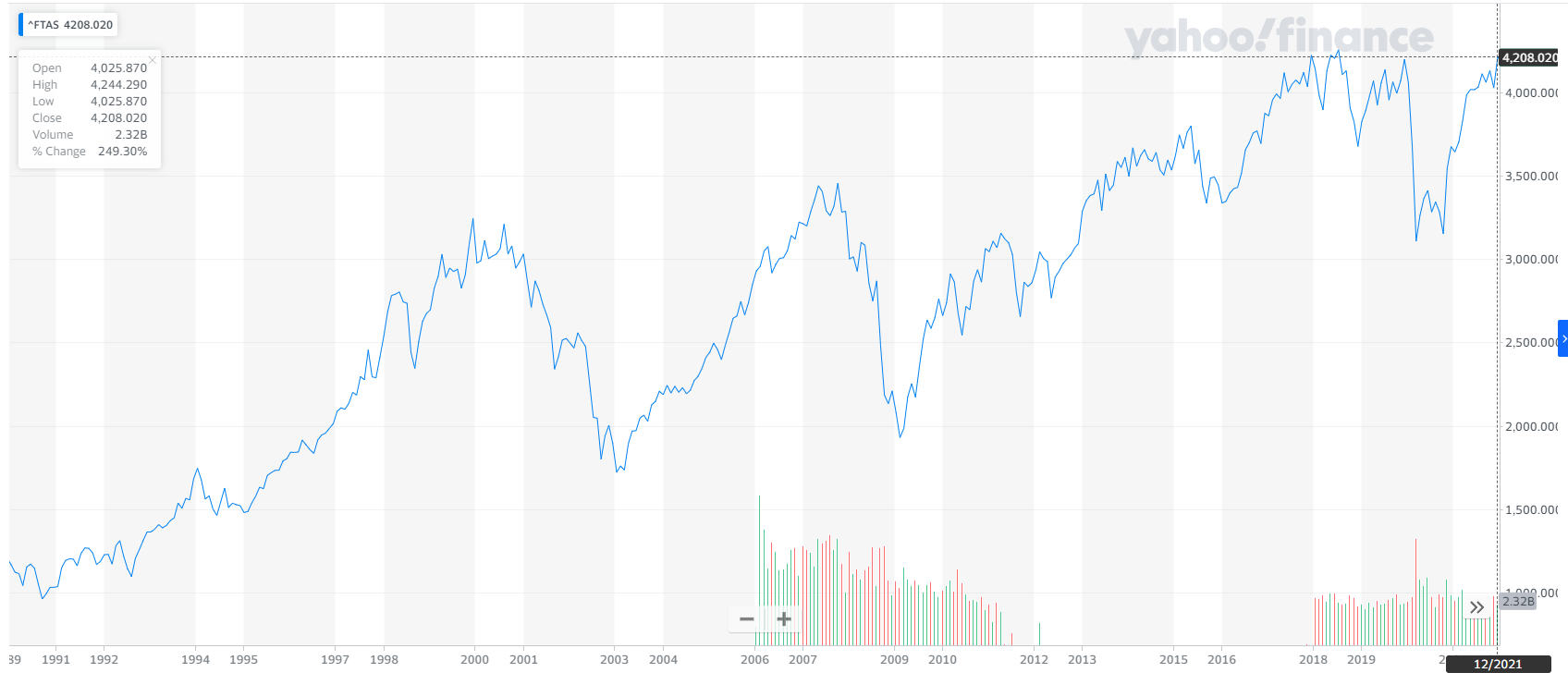

The stock market represents an alternative investment vehicle to property and as we have used UK average house prices, we can use the FTSE All-Share index as a good point of comparison.

As demonstrated above, over the last 22 years residential property has grown by 222% whereas the FTSE All-Share index has grown by slightly more at 249%.

The heady days of property growth from January 2000 to October 2007 saw a rise of 125% versus a comparatively lacklustre 6.5% growth in the same period for the FTSE all share.

The global financial crisis (GFC) caused residential property to drop by 16% from January 2008 to March 2009, whereas the FTSE All-Share was more volatile and dropped 29% in the same period.

In the years following the GFC (2009-2022), property prices grew by 74.5% whereas the FTSE All-Share performed significantly better at 138%.

During the pandemic (Jan 2020 to December 2021), the UK average house price increased by 18.6%, whereas the FTSE All-Share only grew by 3.67%.

FTSE All-Share index 1990 -2022

From the above, we can consider that although both investment types have performed similarly over the last 22 years, residential property saw huge growth in the first decade, whereas the stock market has seen significantly better returns in the second decade, albeit somewhat hampered by the pandemic.

What does the future looks like for property price growth?

In light of the above, it is clear that residential property price growth in the UK had levelled off at a level that is just above inflation, before the tremendous gains during the pandemic which is now starting to cool slightly. Given the recent jump in prices and increasing interest rates, it’s likely that we may revert to slower price growth unless:

The supply of new housing falls dramatically (which is contrary to government policy);

The population suddenly increases;

Average earnings rise significantly;

Unchecked financing opportunities are introduced (which is also unlikely as checks and balances were introduced across the mortgage industry following the GFC).

Furthermore, residential property value increases are likely to be further limited by affordability.

Back in 2000, the average full-time salary was £18,850. Which made the average house at £85k worth 4.5x the average salary.

In 2010 the average full-time salary was £25,880. Which made the average house at £167.5k worth 6.5x the average salary.

In 2019 the average full-time salary was £30,380. Which made the average house at £228k worth 7.5x the average salary.

In April 2021 the average full-time salary was £31,772. Which made the average house at £251k worth 7.9x the average salary

These increased income multiples mean buyers need bigger deposits, a higher income or a higher percentage of income is required to sustain the mortgage payments. Additionally, stamp duty purchase taxes are also a large percentage of income and therefore require longer to save for.

In response to these affordability pressures, the government has artificially reduced their impact:

Introduced ‘help to buy’ to offer a short-term 20% reduction in the purchase price;

Introduced ‘lifetime ISAs’ to give younger savers a boost for a house deposit;

Removed many financial benefits for landlords to reduce the financial viability of residential property;

Reduced the red-tape required to build more homes and is encouraging as much development as possible.

As such, the government is actively trying to suppress house price growth and affordability has reached a level that can’t support meaningful growth. In retrospect, 2000-2008 was totally different and is unlikely to be repeated in the medium term.

What are today’s opportunities for residential property capital growth?

It is clear that the rate at which the value of property was increasing (pre-pandemic) has slowed and given the recent double digit growth it’s likely that the days of passively riding the wave of residential price growth are over. However, opportunities for capital growth do still exist in the residential property market although they are more likely to stem from active investment activities such as:

Seeking below market value and distressed sale opportunities;

Developing properties to add value;

Building House of Multiple Occupation (HMO) businesses and selling them on.

Conclusion

It is certainly true that residential property has offered some staggering returns, however, this was mainly in both a pre-GFC world (where property was affordable and financing was readily available) and during the pandemic (where demand for larger properties pushed average prices up). Since the GFC, the stock market has grown by nearly double the rate that residential property has and, with increasing government pressure to increase the affordability of homes and recent jump in prices, it’s unlikely that we will see gains like this again in the short to medium term.

Did you benefit from property growth pre-2008 and what market conditions do you think need to be present to see returns like that again? Let us know in the comments and be sure to subscribe to our newsletter to get a monthly digest of articles, just like this one.

What’s next?

If you need help or advice with your finances and investment decisions, you can talk through your options with one of our Financial Advisors right here in Tunbridge Wells.

This article offers information about investing and mortgages and should not be taken as personal advice. Think carefully before securing debts against your home. Your home may be repossessed if you do not keep up repayments on your mortgage or any other debt secured on it. Remember that investments can go up and down in value, so you could get back less than you put in. Past performance is not a guide to the future.