Will the UK return to austerity over rising interest rates?

Will the UK return to austerity over rising Gilt rates?

Introduction.

Will the UK return to austerity over rising Gilt interest rates? With government borrowing costs climbing rapidly, this question has become a pressing concern for policymakers and the public alike. The potential return to austerity looms large, and in this article, we'll explore why rising interest rates on government debt are significant, how inflation and economic growth interact with borrowing, and why some fear that these trends could lead the UK back into an era of austerity.

Why are interest rates so important?

A crucial point in understanding government debt is recognising that interest rates determine how much a government must pay each year to service its borrowing. When interest rates are low, debt becomes more manageable. When they spike, keeping up with interest payments becomes significantly more expensive.

Government borrowing refers to issuing UK gilts, which are government bonds sold to investors. These gilts can have varying maturities, such as 5-year, 10-year, or longer-term bonds, and the government pays interest (known as the yield) to those who purchase them. Rising yields on gilts indicate higher borrowing costs, which can strain public finances and influence economic policy.

The 10-year gilt yield is a key benchmark for UK borrowing costs and is often viewed as a reflection of long-term confidence in the economy and government finances. Higher yields on 10-year gilts suggest that the government faces increased costs for funding its operations over the long term, which can significantly impact fiscal planning.

UK 10 year Gilt Source: https://markets.ft.com/data/bonds/tearsheet/charts?s=UK10YG

Recently, the UK's borrowing rate has risen close to 5%. Although rates like this were common before the 2008 financial crisis, the current circumstances are different. The UK's overall debt is larger now, having increased substantially during the pandemic, and economic growth is much lower than in previous decades. This combination makes a seemingly ordinary interest rate of around 5% more worrisome than it used to be.

Inflation, growth, and how they affect debt.

Governments often borrow more than they raise in taxes, yet their debt does not necessarily keep rising indefinitely as a share of the economy. The reason lies in two forces that help boost Gross Domestic Product (GDP):

Economic growth: If a nation's economy grows (for example, by 1% annually), it expands the overall "size of the pie."

Inflation: Rising prices (inflation) cause GDP to increase in monetary terms, even if the real output remains steady.

Meanwhile, the absolute size of the government's debt - what it owes in pounds - remains the same unless more is borrowed. Inflation helps increase GDP each year, which can offset new borrowing. In other words, higher GDP makes debt appear more manageable.

However, the problem arises when the interest rate on government borrowing is higher than the combined boost from economic growth and inflation. If the government faces interest rates of around 5% but overall GDP is only growing at around 3.5% (assuming 1% real growth and 2.5% inflation), debt would grow faster than the economy. Over time, debt as a share of GDP would increase unless the government either raises more through taxes, cuts its spending, or both.

Source: Office for National Statistics, International Monetary Fund World Economic Outlook April 2024.

Why this situation is concerning now.

Over the past decade, the UK has benefited from near-zero interest rates, which have helped keep the debt at a manageable level, even during periods of heavy borrowing post the 2008 crisis and more recently, during the Covid-19 pandemic. However, this low-interest environment has undergone a drastic change. Interest rates are on the rise globally, and in the UK, they have inched closer to 5%, a figure significantly higher than the combined average inflation and growth rates.

This significant gap between the interest rates and the combined average inflation and growth rates implies that unless the government implements policies to boost economic growth or maintain higher inflation, the debt could outpace the economy's growth. Financial markets are quick to notice this, and it can trigger anxiety, leading to spikes in the cost of government borrowing. In extreme cases, this cycle can spiral if investors start to doubt the government's ability to repay its debts.

Will the UK return to austerity?

If the cost of borrowing remains too high, the UK government has limited choices:

Increase economic growth: This is often the ideal solution but difficult to achieve quickly.

Allow higher inflation: This can help reduce the real value of debt, but high inflation has its own harmful consequences for households.

Cut spending or raise taxes: Reducing the deficit is the most direct method, but it comes at the political cost of austerity measures, tax increases, or both.

In the short term, markets often expect quick solutions. Governments that struggle to reassure investors can face intense pressure to reduce public spending. Many fear this could mark a return to austerity policies, which typically involve cuts to public services or social programmes.

Finding this useful?

Once a month, we send our latest articles on pensions, investments, mortgages, protection, estate planning and more - along with a couple you might have missed. Practical reading for anyone taking their finances seriously.

Join our readers →How does the UK compare to other countries?

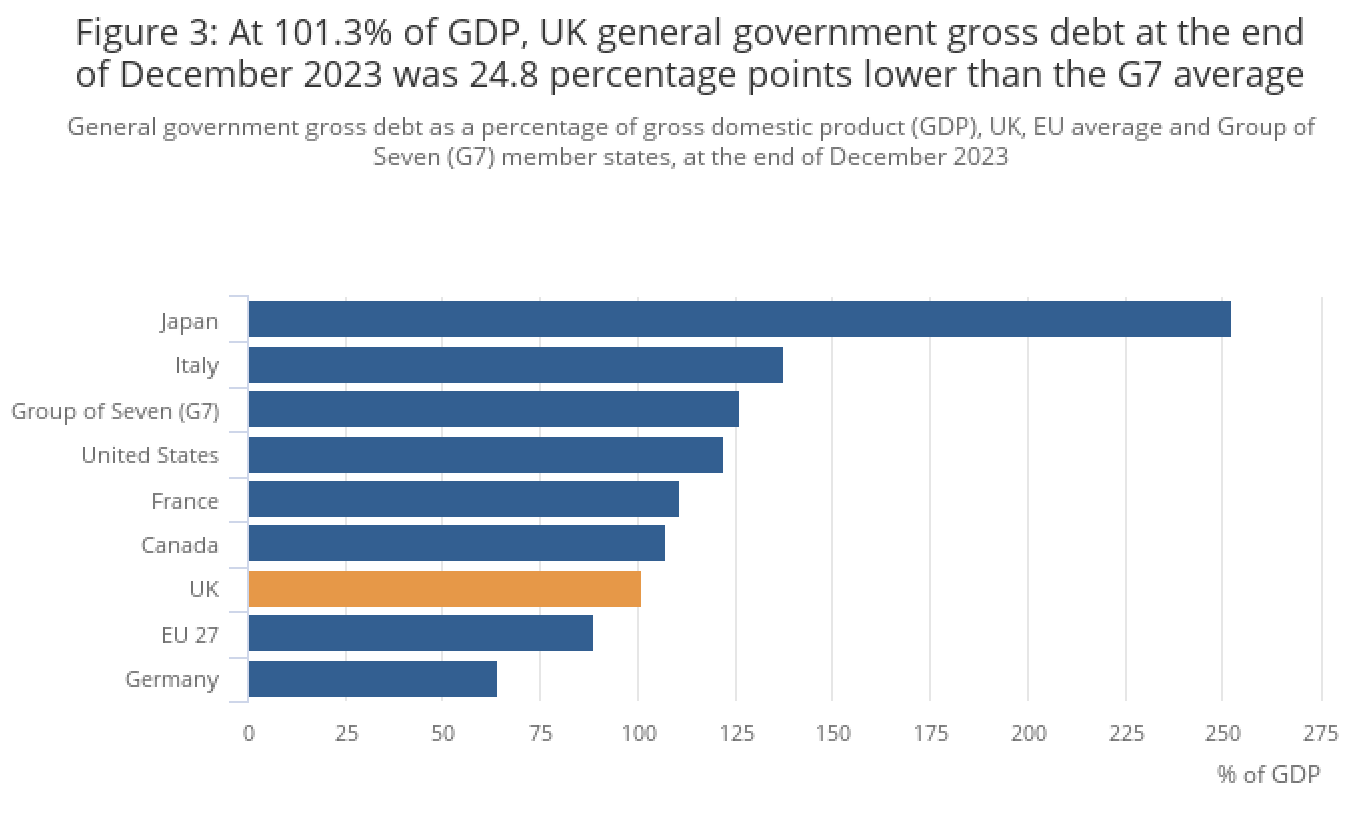

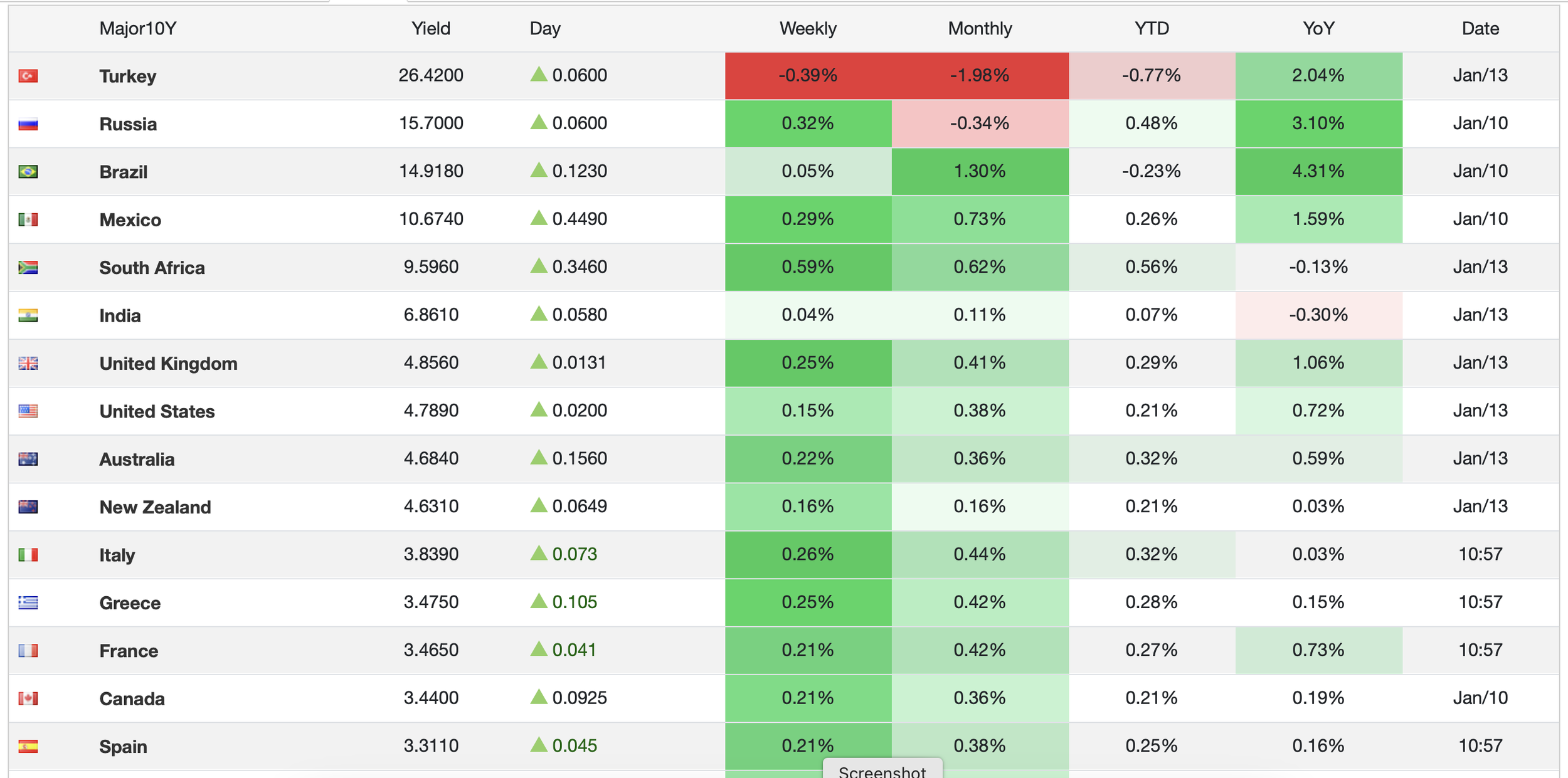

While global interest rates are up everywhere, the UK seems particularly sensitive. Some other European countries, like Italy, currently pay lower rates on their debt (albeit not by a massive margin). This comparatively higher rate for the UK reflects investors' wariness about the UK's economic fundamentals, including slower growth projections and the larger debt pile resulting from pandemic spending.

World bond yields compared ( January 2025). Source: https://tradingeconomics.com/bonds

Where does this leave government policy?

Governments worldwide often try to balance borrowing for public spending and keeping deficits manageable. The importance of a balanced fiscal policy cannot be overstated. If interest rates stay high for a sustained period, the UK may be forced to introduce austerity-like measures or tax rises (or both). Regardless of political persuasion, governments end up with little choice if the market demands better proof of their ability to pay back debt.

Many argue that more should have been done earlier to adjust tax policy and ensure the government did not become too reliant on borrowing. The need for sustainable growth and tax compliance is urgent. Others maintain that extraordinary circumstances, such as the pandemic, required massive state intervention with limited options to recoup the costs until later. Wherever you stand politically, the reality is that higher interest costs push the UK into a position where painful decisions may lie ahead.

What are some potential solutions to the problem?

With higher earners and businesses already facing significant tax increases under the current government—including hikes in corporation tax, national insurance, capital gains tax, and measures targeting private schools—further squeezing these groups could risk dampening growth and stoking public discontent. Balancing fiscal policy effectively requires a careful approach that avoids overburdening taxpayers while addressing rising borrowing costs. Here's a breakdown of realistic solutions and actions to avoid for the UK government.

Five realistic measures to improve the UK’s fiscal stability.

Invest in growth sectors: Direct funding towards renewable energy, technology, and infrastructure projects that boost productivity, create jobs and generate long-term tax revenues. These investments can strengthen the economy without the immediate need for further tax hikes.

Tackle tax evasion and avoidance: Strengthen enforcement mechanisms to improve tax compliance among large corporations and high-net-worth individuals. The government could generate substantial revenue by closing loopholes and recovering unpaid taxes without introducing new tax burdens.

Streamline public spending: Conduct a thorough review of government programmes to identify inefficiencies. Redirecting funds from wasteful or redundant initiatives to priority areas can help reduce the deficit while maintaining public services.

Encourage private sector partnerships: Leverage public-private partnerships (PPPs) for large-scale projects like infrastructure development. This approach spreads the financial burden and accelerates economic benefits without adding excessive debt.

Stabilise borrowing costs: Maintain fiscal discipline and reassure financial markets with credible, transparent debt-reduction plans. Stabilising gilt markets can reduce borrowing costs and ease pressure on public finances.

Five measures to avoid (but might still be considered).

Excessive reliance on middle-income taxpayers: Further tax increases on middle-income earners risk dampening consumer spending, which is vital for economic growth. This approach could also alienate a broad voter base.

Cuts to essential public services: While spending reductions might offer short-term fiscal relief, cuts to healthcare, education, or infrastructure could harm long-term economic prospects and social welfare.

Selling off national assets: Liquidating public assets such as land or state-owned companies may provide quick cash but sacrifices long-term revenue streams and strategic control over key sectors.

Allowing inflation to devalue debt: Relying on inflation to erode debt could destabilise household budgets, discourage investment, and increase the cost of living, exacerbating existing challenges.

Indiscriminate business tax increases: Blanket tax hikes on businesses could deter investment, stifle innovation, and slow job creation, particularly in globally competitive sectors.

Conclusion.

The key lesson is that rising interest rates are making it more expensive for the UK government to service its debt, raising the question of whether this could lead to a return to austerity. Compared to periods of cheaper borrowing, the current environment places significant pressure on public finances. If interest rates stay higher than the combined effect of economic growth and inflation, the UK's debt could grow faster than its economy, prompting concerns about financial sustainability.

As such, the situation could force difficult fiscal choices. This may mean higher taxes, reduced public spending, or both for ordinary citizens. Whether austerity becomes unavoidable depends on how interest rates evolve and how the government addresses these pressures.

Balancing the fiscal books in the current climate is challenging but necessary. By prioritising sustainable growth, tackling tax avoidance, and improving public spending efficiency, the government can address fiscal pressures without further burdening those already contributing heavily. Avoiding short-sighted measures like deep service cuts or indiscriminate tax hikes will be critical to maintaining economic stability and public trust. A measured approach is essential to avoid stifling growth while navigating the UK's fiscal challenges.

The months ahead will be critical in determining the government's response. Markets will be watching closely, and policymakers must strike a delicate balance to avoid undermining public confidence or creating long-term financial strain.

What’s next?

Wherever you are in the UK, we invite you to book a free initial consultation with one of our experienced financial advisers. Whether you’re concerned about the economic outlook, managing your investments, planning for retirement, or better understanding pensions, we provide expert advice tailored to your needs. Based in Tunbridge Wells, Kent, we proudly serve clients nationwide.

Locally, we serve clients across Kent, including Ashford, Maidstone, Sevenoaks and Tonbridge. In East Sussex, we have clients in Bexhill, Crowborough, Eastbourne, Hastings, Heathfield and Uckfield.

Don't forget, this article offers general financial information and should not be taken as personal advice. Remember that investments and pensions can go up and down in value, so you could get back less than you put in. Tax rules can change and will depend on your individual circumstances.