What are the costs of care in the UK?

Social care can be expensive. Knowing how much you may have to pay will help you budget and plan ahead. Social care systems in England, Wales, Scotland and Northern Ireland operate in different ways – this article focuses on the costs and operation of adult social care in England.

What is adult care in the UK?

Adult care, or social care, covers a wide range of activities to help people who are older or living with disability or physical or mental illness live independently and stay well and safe.

It can include care in your own home, in a care home or nursing home or even in a hospital. Support will include help with washing, dressing, preparing food and getting out of bed in the morning, as well as wider support to help people stay active and engaged in their communities.

The number of people who need social care has risen over recent years: 1.9 million people requested support from their council in 2019/2020, an increase of more than 100,000 over the previous 5 years.

How much does social care cost?

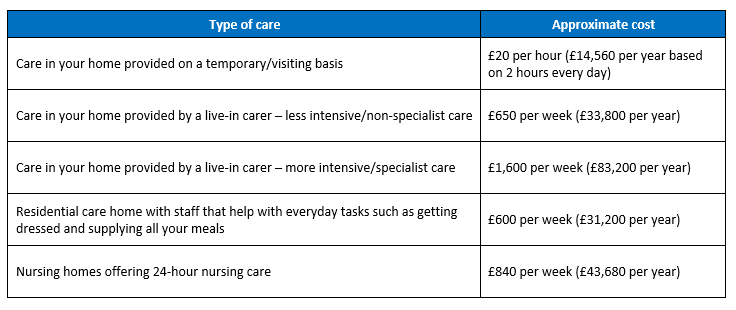

Costs will vary depending on where you live (which local authority you are in) and the type of care you need, but the following will give you a good idea of what it could cost:

The costs of social care in England

For people who fund their own care the Competition and Markets Authority estimated that care home fees are, on average, 41% higher than those paid by local authorities for places in the same care homes. This would increase the costs above as follows:

The costs of care homes for people who are self-funding

How much is the cost of care over someone’s lifetime?

The lifetime cost of adult social care varies considerably according to the level of need. In 2010 the Dilnot Commission estimated:

50% of people aged 65 and over will spend up to £20,000 on care costs; and

10% would face costs of more than £100,000.

However, costs are very hard to prepare for not least because it is almost impossible to predict who will require care and to what extent. For example, trying to predict who will develop dementia, as the majority of dementia conditions are not hereditary.

Who is eligible for publicly funded social care in England?

Most publicly funded social care in England is only available to people with the highest needs and lowest assets – assets include your savings and, for residential care, the value of your home.

If you have no savings or savings of less than £23,250, your council might be able to help with the cost of care. The first step is for them to complete a financial assessment. If when you start receiving care you have savings of more than £23,250 and they subsequently fall below this level you can contact them to be re-assessed at that time, although it’s always better to contact them before your savings fall below that level if you think you are going to need help.

You can read more about the financial assessment on the NHS website.

You can choose to pay for care yourself if you don't want a financial assessment.

How to find out what care you need.

Even if you choose to pay for your care yourself, your council can do an assessment to check what care you might need. This is called a needs assessment.

For example, it will tell you whether you need help at home from a paid carer for 2 hours a day or 2 hours a week and precisely what they should help you with.

The needs assessment is free and anyone can ask for one. You can find out more about arranging a needs assessment on the NHS website.

Are there any state benefits that can help with care costs?

There are some state benefits which are not means-tested, which may be able to help you pay for the costs of care, such as Attendance Allowance and Personal Independence Payment (PIP).

Read about benefits for under-65s on the NHS website.

Read about benefits for over-65s on the NHS website.

What is a deferred payment scheme?

A deferred payment scheme is an arrangement whereby the person needing care agrees with their local authority to pay some of their care fees at a later date. This means they should not be forced to sell their home during their lifetime, to pay for their care. The person usually repays the local authority from the sale of their property or it is repaid from their estate after their death.

A deferred payment scheme can be useful if you have savings of less than £23,250 and all your money is tied up in your home.

What you can get for free.

You might be able to get some free help regardless of your level of savings or income or if you're paying for your care.

This can include:

Small bits of equipment or home adaptations that each cost less than £1,000

NHS care, such as NHS continuing healthcare, NHS-funded nursing care and care after you have been discharged from hospital

Read more about care and support you can get for free on the NHS website.

What are the funding options for care fees?

Much of the care provided by local authorities is means-tested. This means that many people will have to self-fund their care, in whole or in part. This is normally done in one or several ways:

Taking lump sums and/or income from pensions, savings and investments

Using the rental income from an investment property

Using the equity within your home via an equity release plan

Gaining financial support from family members

Using capital to buy a long-term care plan (either ‘immediate needs’ or ‘deferred needs’)

Using pre-funded long term care insurance

What next?

We’ve put together a free guide that fully explains the complex topic of social care and care fees.

If you would like to discuss any of the issues highlighted in this article or to explore the options available to you for funding your current or future care fees, please get in touch. An initial chat is free and our experienced and knowledgeable Independent Financial Advisors will be happy to help.

This article offers information about financial planning and should not be taken as personal advice.