What are Investment Pathways? A summary of your options.

Investment Pathways are a way for people to access their pensions and are available from February 2021. They were designed specifically for people who do not want to take financial advice. To get a better understanding of what they are and how they came about, let’s first look a bit more at what happens when we reach a certain age in terms of our pensions and retirement plans.

When can I access my pension?

When we reach age 55 most of us are able to access our pensions in a way which suits our future retirement plans. Age 55 is the minimum legal age we can do this (although this is going to increase in the future to age 57) when we have what is known as a defined contribution (DC) pension. DC pensions differ to defined benefit (DB) – or final salary – pensions, in that what we get back at the end is based largely on what we, plus our employer and the government through tax relief, pays in, as well as how well the pension investments have performed. The final bit of the puzzle is how we choose to take the money out of our pension.

There is no maximum age limit that you can choose to access your DC pensions, so if you don’t want to make a choice at age 55 you don’t have to.

Because historically pensions typically had a set retirement age of 65, your pension provider is likely to contact you at that age to ask you what you want to do. But again, you do not have to do anything if you’re not ready, say because you’re still working, or because you have other savings and investments you’re living off and therefore don’t yet need your pension.

What are my options when I retire?

Since the Pension Freedoms were introduced in 2015, there has been far more choice in how we can access our pensions. Broadly speaking, they are:

Buy a guaranteed income (an annuity) – where the payments are taxed as income (you can take 25% of the value of your pension first, tax-free).

Arrange ‘flexible drawdown’, where lump sums or regular payments can be drawn down from your pension – you can take just the 25% tax-free lump sum at first and then start taking an income or ad hoc withdrawals which will be subject to income tax.

Take the whole amount as a lump sum – where 25% is tax-free and 75% is taxed as income (the 75% is added to your other taxable income in that tax year to work this out, so you may pay much more tax and at a higher rate than you expect to).

Take a number of lump sums out of your pension – where each withdrawal is 25% tax free and 75% is taxed as income.

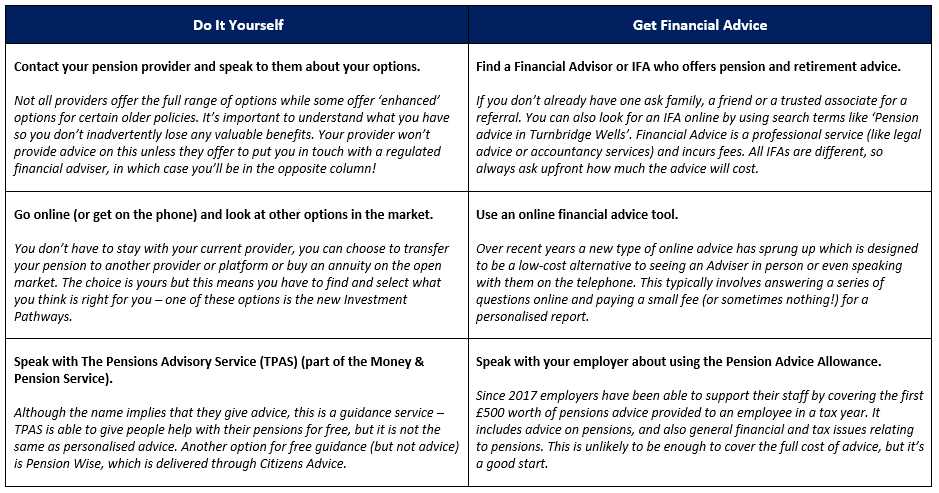

Do I need to get financial advice when I retire?

The simple answer is no. When you retire, or are thinking about retiring, you can either do it yourself or you can get advice. Within each of these options there are typically several choices, which we’ve summarised below:

Useful links:

The Pensions Advisory Service (TPAS) (part of the Money & Pension Service).

Pension Wise (delivered through Citizens Advice).

Learn about the costs of financial advice in our full article on The Cost of Financial Advice.

How do Investment Pathways fit in?

As shown above, Investment Pathways are designed for people who don’t need or want financial advice. This means you need to make an active choice about what it is you want. The starting place is deciding what you are trying to achieve. The Investment Pathways are designed with that starting point in mind. They are a set of four prescribed retirement objectives as set out below. The starting point is the same for every provider that offers them, but how they deliver them, i.e. the underlying investment strategies, will be specific to that provider including where the money is invested and how much those investments cost.

The four Investment Pathways:

Pathway 1: I have no plans to touch my money in the next 5 years

Pathway 2: I plan to use my money to set up a guaranteed income (annuity) within the next 5 years

Pathway 3: I plan to start taking my money as a long-term income within the next 5 years

Pathway 4: I plan to take out all my money within the next 5 years

Why were Investment Pathways introduced?

The UK’s financial regulator, the Financial Conduct Authority (FCA), previously expressed concern about consumers moving into drawdown at retirement (without taking financial advice) and holding their funds in investments that will not meet their needs. The FCA believes that by introducing Investment Pathways, it will help non-advised drawdown consumers select from four relatively simple choices, designed to meet their broad retirement objectives so that they can maximise their income in retirement.

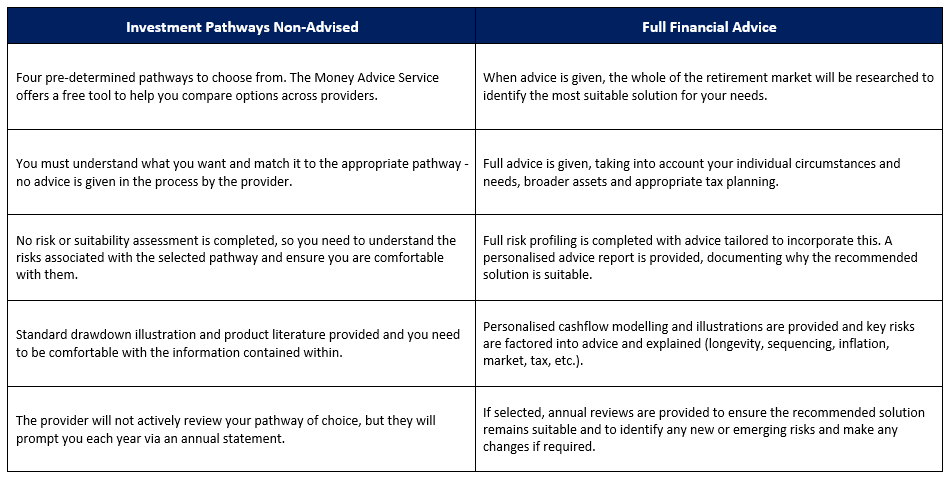

Can I get advice on Investment Pathways?

Investment Pathways are specifically designed for people who do not want or need financial advice. However, that does not mean you can’t get advice on them. You can speak to your existing Financial Adviser about them or find an IFA for this purpose. However, good IFAs will provide their advice based on a full assessment of your circumstances and needs. This may or may not include Investment Pathways (although if relevant it should give them due consideration).

We have summarised below what we believe the key differences are between using Investment Pathways without advice (as they were designed to be used) and seeking full financial advice from an independent whole of market IFA (like AV Trinity).

Useful links:

The Money Advice Service Investment Pathways comparison tool.

How we can help

We have many years’ experience of providing advice on pensions, retirement planning and the associated areas of advice, such as tax, estate planning, equity release and long-term care. As Chartered Financial Planners, we are at the forefront of the financial advice profession. You can learn more about what this means in our article on being a Chartered Financial Planner.

Get in touch for a free initial chat.

Please note this article offers information about financial planning and should not be taken as personal advice. The value of pensions can go up and down in value, so you could get back less than you put in. Tax rules can change and the benefits depend on individual circumstances.