How to save serious money on your mortgage.

Even though we are living through a period of record low interest rates, our old friend compound interest can still come into play with mortgages.

If there was one takeaway from our earlier article, it’s that small amounts over a long period of time can really add up. This can either work for you by investing the money, or against you by paying interest on a loan.

How a shorter mortgage term saves you money.

To kick off, let’s look at the average first-time buyer mortgage.

According to UK Finance, the average first-time buyer is 32 years old and borrows about £175,000 for their first mortgage with a loan to value ratio (LTV) of 77%. This makes the average first property worth about £227,000. It is also worth noting that the average first-time buyer borrows with an income multiple of 3.5; therefore the average first-time buyer earns a much higher than average salary of £50,000.

Many first-time buyers’ mortgages are taken out for 30-years and current interest rates for a 5-year fixed rate are around 2.25%.

Let’s imagine our average first-time buyer buys this house, never moves and interest rates stay the same. The monthly payment would be about £670 and the total interest payable on the loan (ignoring any fees that may be payable) would be £65,000. This means the mortgage company would make a theoretical 37% profit over 30-years.

Keeping all the variables the same, except reducing the term to 25-years, the monthly repayment would be about £100 more each month at £760. However the total interest paid over the mortgage term would be just shy of £54,000. That’s £11,000 saved over taking out a 30-year mortgage.

Let’s stay with this and adjust the mortgage term to 20-years. In this example, the repayment would jump to £906 per month, with a total interest amount payable of about £42,000. This is a further reduction of £12,000 over a 25-year mortgage and a huge £23,000 saved in interest when compared to the 30-year mortgage.

Finally, let’s imagine the buyer was really keen to be mortgage free as soon as possible and went for a 15-year mortgage. The monthly repayment would be about £1,150 each month and the total interest paid over that 15-year period would only be about £31,000 – less than half the interest paid on a 30-year mortgage term.

The key takeaway from this exercise is that your ability to absorb a slightly higher monthly repayment (often a few hundred pounds) can dramatically reduce your mortgage term and save tens of thousands of pounds over the longer term.

The figures get even bigger for house movers and remortgages.

UK Finance suggest that the average mortgage loan for a house-purchaser (who is already on the ladder) is about £231,000. In this case, if the term is 25-years and the mortgage rate is similar at 2.5%, the monthly repayment would be just over £1,000 each month and about £71,000 total interest paid.

As you can see, the larger loan has a magnifying effect on the interest paid.

If this buyer was able to accept a slightly higher monthly repayment of £1,200 for a mortgage term of 20-years, the total interest paid would drop by a staggering £15,000 to £56,000. Interestingly, if they were able to pay in the region of £1,500 each month, the term would drop to 15-years and the total interest paid would be a little over £41,000, saving the buyer £30,000 over a 30-year mortgage term.

I’m already tied-in to a mortgage, how can I save money?

Depending on the conditions of your mortgage, you may be able to overpay a significant amount each month to reduce the term and save interest.

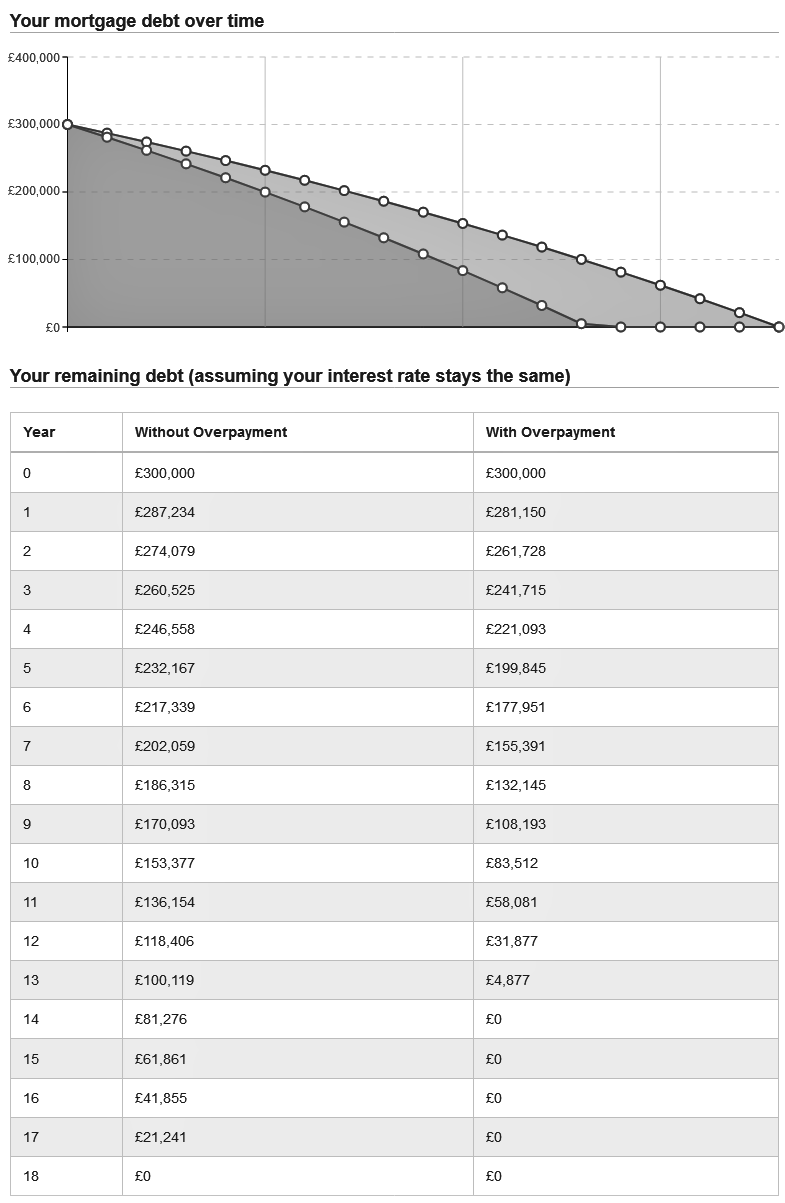

Let’s say you have a £300,000 balance on your mortgage, with 18-years left to run and your interest rate is 3%. Your monthly repayment is likely to be in the region of £1,800 and, if you just carried on as normal, you will pay approximately £88,000 in interest over the next 18-years.

If you committed to overpaying your mortgage each month by just £200, you would save about £12,000 in interest and pay off your mortgage 2-years and 3-months earlier.

That’s a big gain for the cost of a couple of good meals out each month.

Furthermore, if you really decided to tighten your belt (or had a reasonable pay-rise) and you could free up £500 extra each month from your budget to put towards mortgage overpayments, you would save over £25,000 in interest and clear your mortgage 4-years and 9-months earlier. Here’s how that looks:

Example of a mortgage overpayment calculation, courtesy of moneysavingexpert.com.

What’s next?

Obviously everybody’s circumstances are different and you will need to check with your mortgage provider the overpayment terms, however it is worth having a play with the many mortgage tools out there to see the money you could save, like this mortgage overpayment calculator and this mortgage loan calculator.

Alternatively, you can speak through your options with one of our mortgage brokers right here in Tunbridge Wells.

This article offers information about mortgages and should not be taken as personal advice. Think carefully before securing debts against your home. Your home may be repossessed if you do not keep up repayments on your mortgage or any other debt secured on it.