What is Pension Tax Relief?

Pension tax relief is a ‘bonus’ paid by the government on money someone pays into their pension. At present, how much tax relief you receive is dependent on what you earn and what your highest rate of income tax is. This may change in the future with many speculating that it could become a single flat rate for everyone who is eligible.

This article relates to how tax relief operates on pension contributions made by individuals in the UK at the present time. The tax treatment of employer contributions will be covered in a future article.

Who can pay into a pension?

Pension contributions can be paid by:

An individual who has a personal pension or is a member of a workplace pension scheme.

That individual's employer.

A third party on behalf of that individual (such as a grandparent for their grandchild).

Tax relief is given on contributions paid during a tax year. They must be a monetary amount and paid for example, by cheque, bank transfer or direct debit.

There is technically no limit to the amount that can be paid into a pension. However, there are limits to the amount of tax relief that can be obtained on those contributions.

Who is eligible for tax relief?

Tax relief is available to individuals who are:

Under age 75; and

Who are classed as a ‘relevant UK individual’.

A relevant UK individual must meet one of the following conditions:

Have relevant UK earnings chargeable to income tax for that tax year,

Are resident in the UK at some time during that tax year,

Were resident in the UK at some time during the five tax years immediately before the tax year in question and they were also resident in the UK when they joined the pension scheme, or

Have for that tax year general earnings from overseas Crown employment subject to UK tax (as defined by section 28 of the Income Tax (Earnings and Pensions) Act 2003), or

Are the spouse or civil partner of an individual who has for the tax year general earnings from overseas Crown employment subject to UK tax (as defined by section 28 of the Income Tax (Earnings and Pensions) Act 2003).

Relevant UK earnings

The levels of tax relief available depend on the individual's relevant UK earnings in the current tax year. Generally speaking, all earned income (for example, income from employment) is relevant earnings. The main earnings which are not included are pension income, dividends and most property rental income. For self-employed individuals, their relevant earnings are profits calculated over their chosen accounting period.

You can obtain the full definition of relevant UK earnings from the HMRC’s Pensions Tax Manual.

Level of tax relief

Tax relief is available on the following contributions:

UK residents – the greater of £3,600 gross and 100% of relevant UK earnings.

Non-UK residents – £3,600 gross.

The £3,600 amount is known as the 'basic amount'.

There is another ‘cap’ in place called the Annual Allowance, which for most people is £40,000 per tax year. If someone’s relevant earnings exceed this then the Annual Allowance will be the overall cap. This is a complex point in itself and we will explore this in detail in a further article.

Basic rate taxpayers

Anyone under age 75 can benefit from basic rate tax relief on some or all of the contributions they pay, regardless of whether or not an individual actually pays any income tax.

If an individual has relevant earnings of less than £3,600 per year, or they have zero relevant earnings, they can still pay up to £2,880 to a personal pension each tax year and they will receive £720 of tax relief, making a total gross contribution of £3,600.

Higher and additional rate taxpayers

Higher and additional rate taxpayers are entitled to tax relief at their highest marginal rate of income tax. The tax relief is limited by the amount of an individual's income that falls within the higher or additional rate tax bracket.

How to claim tax relief

The two most common ways to claim tax relief are:

The net pay method

The relief at source method

We will look at each of these in turn.

Net pay

This method is used by trust-based (‘occupational’) employer-sponsored pension schemes. An individual’s pension contributions are deducted from their salary before tax is calculated. Although the pension contribution doesn’t therefore get taxed, National Insurance will still apply on the overall salary.

For example, where an individual wants to pay £100 per month into their pension, the employer would deduct the £100 from their pay each month and pass it to the pension scheme. That £100 doesn’t get taxed by the employer and therefore is treated as having received tax relief at the individual’s highest tax rate – so, if the individual is a basic rate taxpayer the tax relief would be £20 (20%), if they pay higher rate tax it would be £40 (40%), and if they paid additional rate tax it would be £45 (45%). This is classed as a gross pension contribution of £100.

Relief at source

This method is used by personal pensions, stakeholder pensions and employer-sponsored group personal pensions. If an individual is paying into their company’s group personal pension scheme, the pension contribution is deducted from their salary after tax is calculated and deducted.

If an individual is paying into their personal pension, the contribution is paid from their bank account.

The contributions are treated as being paid net of basic rate tax relief and the pension scheme administrator claims basic rate tax relief from HMRC, which is paid directly into the pension scheme.

For example, for every £80 paid by the individual, HMRC adds £20 in tax relief to make a £100 gross contribution. The addition of the tax relief is known as ‘grossing up’.

If the individual is entitled to a rate of tax relief above the basic rate, they must claim this from HMRC via self-assessment.

It’s important to remember that individuals will only get a rate of tax relief above basic rate for any taxable income above the basic rate. For example, someone with £1,000 of earnings in the higher rate of tax paying £10,000 gross into a pension scheme each year would only be able to reclaim higher rate relief for the £1,000 that is in the higher rate band of tax, not the full £10,000.

Due to the way tax relief operates those with earnings of less than £3,600 a year or those with no earnings can only make use of the £3,600 contribution referred to earlier if paying to a pension scheme that uses the relief at source method.

If a self-employed individual makes a pension contribution for themselves, this is treated for tax purposes in the same way as any other personal contribution as outlined above.

Is tax relief instant?

Yes for the net pay method. For relief at source, it can take up to 10 weeks for the pension scheme provider to receive the basic rate tax relief from HMRC. However, many pension scheme providers will usually gross up the contribution immediately at the time the net contribution is received at their own cost and retrospectively claim the tax relief from HMRC to cover this cost.

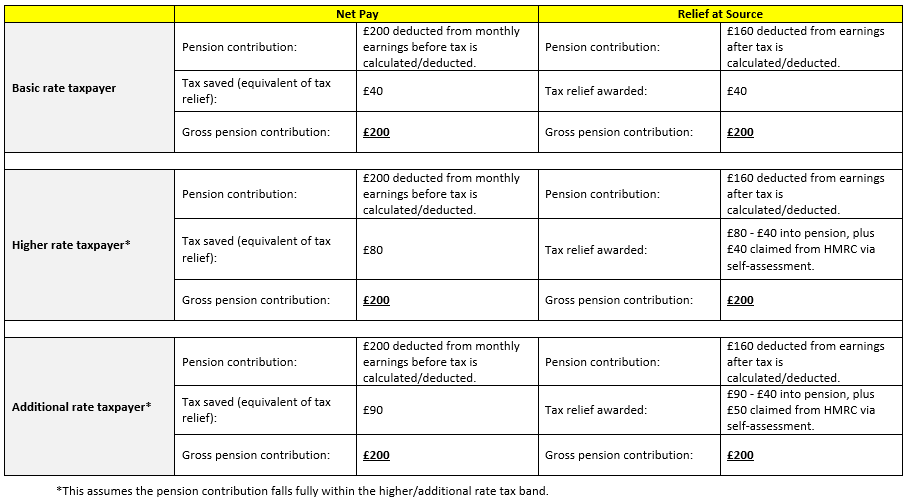

Some example calculations - for an individual making a gross pension contribution of £200.

As can be seen from the above examples, tax relief can be very beneficial regardless of which method is used by the pension scheme. If your company pension offers you to pay your contributions via salary sacrifice or salary exchange, this can sometimes achieve even greater savings. This is not covered here but we will cover that in a future article.

Summary

Paying into a pension is a tax-efficient way of saving for retirement – there are very few investments which exist in the UK which allow tax to be saved on the way in, in this case via tax relief on contributions.

If you’d like to learn more about pensions, get in touch to speak with one of our IFAs to see how we can help.

This article offers information about pensions and should not be taken as personal advice. Please note, tax rules can change, and the benefits depend on individual circumstances. Pensions are a form of investment and they can go up and down in value, so you could get back less than you put in.