How will higher interest rates affect my mortgage repayments?

How will higher interest rates affect my mortgage repayments?

Introduction.

It won’t come as a surprise to homeowners with mortgages that interest rates keep on rising and to a level not seen for a very long time. Whether you are on a variable rate mortgage and your monthly payments keep increasing or perhaps you took out a fixed-rate deal and you are concerned about what will happen when your fixed-term deal comes to an end; either way, anyone with a mortgage will likely be affected at some point by increased interest rates.

In this article, we'll consider what impact higher interest rates will have on your monthly repayments by running some examples through a mortgage repayment calculator.

Understanding the impact of higher interest rates.

To fully understand the implications of higher interest rates on your mortgage repayments, it's essential to understand what interest rates are. The Bank of England sets a base interest rate to (in theory) increase or decrease demand in the economy in order to boost or dampen inflation. Mortgage lenders then adjust the interest paid on loans (mortgages etc.) and deposits (savings accounts etc.) accordingly. Generally speaking, when interest rates increase, borrowing money becomes more expensive and vice-versa.

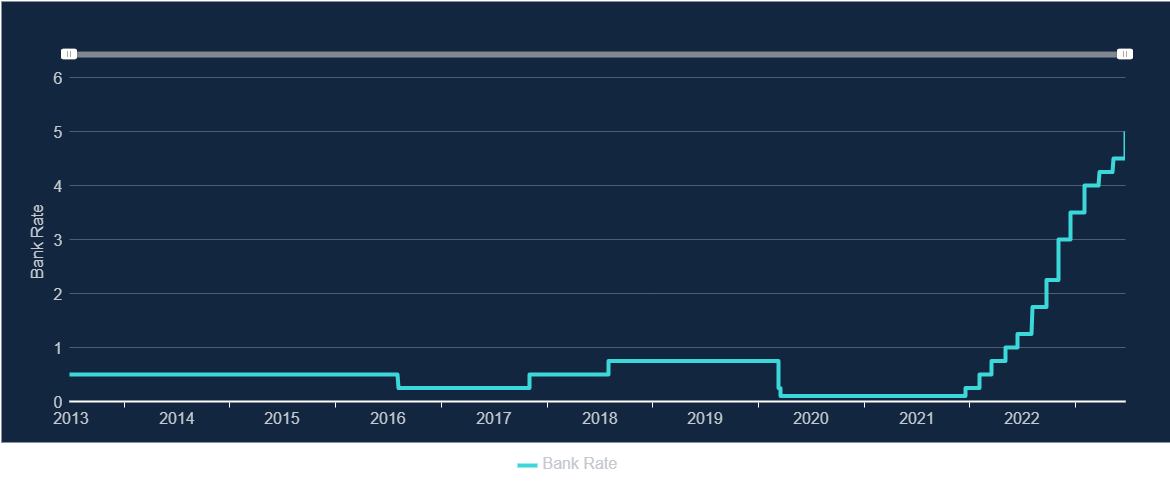

For the last decade, the Bank of England’s base rate has fluctuated at less than 1%. This made borrowing historically cheap and has driven incredible growth in property values in recent years. However, at the time of writing, the Bank of England had increased their base rate to 5% in a little over 1 year.

Bank of England base rate over 10 years. Source: Bank of England.

So, how does this affect your mortgage repayments? The interest rate on your mortgage is a crucial component of your monthly payments. As interest rates rise, the cost of borrowing also increases. Now, let's explore the potential effects of higher interest rates on your mortgage repayments.

Real-world examples of the impact of increased interest rates.

Example 1: You took out a 28-year repayment mortgage for £455,000 with a fixed interest of 1.35% for 5 years. Your current mortgage repayment is £1,633 each month.

By the time your 5-year fixed-rate deal ends, there will be 23 years left to run and an approximate balance of £388,000. In this example, it’s clear that current interest rates could add over £1,000 each month to the homeowner’s mortgage repayment.

|

Interest Rate |

Repayment |

Extra |

|

1.35% |

£ 1,633.00 |

£ - |

|

2% |

£ 1,755.00 |

£ 122.00 |

|

3% |

£ 1,948.00 |

£ 315.00 |

|

4% |

£ 2,152.00 |

£ 519.00 |

|

5% |

£ 2,369.00 |

£ 736.00 |

|

6% |

£ 2,596.00 |

£ 963.00 |

|

7% |

£ 2,832.00 |

£ 1,199.00 |

|

8% |

£ 3,079.00 |

£ 1,446.00 |

23 year/£388k repayment mortgage.

Example 2: You took out a 20-year repayment mortgage for £250,000 with a fixed interest of 2.1% for 2 years. Your current mortgage repayment is £1,277 each month.

By the time your 2-year fixed-rate deal ends, there will be 18 years left to run and an approximate balance of £229,000. Even though the mortgage loan is substantially less in this example and the original interest rate was not as low, a substantial increase in mortgage interest rates will still add several hundred pounds extra each month.

|

Interest Rate |

Repayment |

Extra |

|

2.10% |

£ 1,277.00 |

£ - |

|

3% |

£ 1,373.00 |

£ 96.00 |

|

4% |

£ 1,488.00 |

£ 211.00 |

|

5% |

£ 1,610.00 |

£ 333.00 |

|

6% |

£ 1,736.00 |

£ 459.00 |

|

7% |

£ 1,868.00 |

£ 591.00 |

|

8% |

£ 2,004.00 |

£ 727.00 |

|

9% |

£ 2,144.00 |

£ 867.00 |

18 year/£229k repayment mortgage.

You can play around with your own figures using our Mortgage Repayment Calculator.

What can you do when faced with increased mortgage repayments?

When faced with higher interest rates, it becomes crucial to reassess the affordability of your mortgage. The increased monthly repayments may strain your budget, leaving less room for other expenses and financial goals. Take stock of your current financial situation and evaluate whether you can comfortably manage the higher mortgage repayments without sacrificing essential aspects of your life.

Although higher interest rates can seem daunting, there are steps you can take to minimise their impact on your mortgage repayments:

Budget Review: Assess your budget to identify areas where you can potentially cut costs or redirect funds towards your mortgage repayments.

Emergency Fund: Maintain an emergency fund to provide a financial cushion for unexpected expenses and to help cover your mortgage repayment in leaner months.

Extra Repayments: Consider making additional repayments before your fixed-rate mortgage comes to an end to reduce the overall interest cost and shorten the loan term.

Seek Professional Advice: Consult with a mortgage broker or financial advisor to explore your options and determine the best course of action based on your circumstances.

Conclusion.

As interest rates rise, it's natural to have concerns about the impact on your mortgage repayments. However, by understanding the potential effects and taking proactive steps, you can navigate these changes confidently. Whether it involves reassessing affordability, tightening your budgets, maintaining a cash fund to help your increased costs or making additional repayments to reduce the overall balance, being well-informed empowers you to make decisions aligned with your financial goals. Remember, while interest rates may fluctuate, careful planning and a proactive approach to managing your finances can take the shock out of increased repayments. As ever, forewarned is forearmed.

What’s next?

If you need help or advice on your mortgage, personal or business finances or if you want to consider investing to make your money work harder, you can get in touch with one of our advisors for independent financial advice. We offer a free initial consultation and although we are based in Tunbridge Wells, we advise clients across the UK.

Don’t forget, this article offers information about mortgages and property and should not be taken as personal advice. Think carefully before securing debts against your home. Your home may be repossessed if you do not keep up repayments on your mortgage or any other debt secured on it.