What is the triple lock on State Pensions and why is it being suspended?

The government has this week announced the triple lock on State Pensions is being suspended. This article explores what the triple lock is and the impact its suspension will have on the State Pension people receive.

What is the triple lock?

The full State Pension is currently £179.60 per week. You may receive more or less than this depending on when you reached State Pension age and depending on your National Insurance record.

If you’re not yet receiving your State Pension, you can check how much State Pension you will receive in future by getting your State Pension forecast.

Once you start receiving your State Pension, it will increase each year by what is known as the triple lock. This was introduced in 2010 by the Conservative/Liberal Democrat coalition government.

The triple lock means State Pensions in payment will increase each year by whichever is the highest of:

Earnings – the average percentage growth in wages (in Great Britain)

Prices (inflation) – the percentage growth in prices in the UK as measured by the Consumer Prices Index (CPI)

2.5%

If you have a ‘protected payment’, it increases each year in line with the CPI. The protected payment is not available to everyone, and will depend on if you started accruing State Pension entitlement before 6 April 2016 (but have a State Pension age after that date) and how much that entitlement was in relation to the full new State Pension.

Prior to the introduction of the triple lock, State Pensions increased each year by inflation.

Is the State Pension triple lock staying?

In its 2019 election manifesto, the Conservative Party said it would keep the triple lock in place for the duration of this Parliament.

However, they are now stating that due to the impact of the coronavirus pandemic (which they could not predict in 2019), this promise cannot be kept for this coming year. If it was kept, it would result in State Pensions increasing by a record amount thanks to artificially high earnings growth – by more than 8% thanks to the effects of the furlough scheme, according to the Office for Budget Responsibility (OBR).

How much will State Pensions increase by next year?

Instead of the triple lock, there will instead be a comparison between Prices (inflation) and 2.5%. Whichever is highest will determine how much people’s State Pension will increase by. This means State Pensions will increase by at least 2.5%.

How much will your State Pension be in 2022?

Based on an increase of at least 2.5%, this means those who are already in receipt of their State Pension will receive at least the following from next April:

If you reached State Pension age after 6 April 2016, you will be receiving the ‘New State Pension’. The full amount (excluding any protected payment) is currently £179.60 a week which will increase to at least £184.10.

If you reached State Pension age before 6 April 2016, you will be receiving the ‘Basic State Pension’. The full amount is currently £137.60 a week which will increase to at least £141.05.

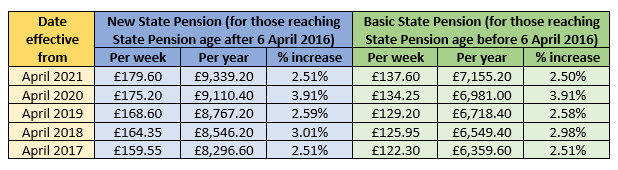

How much did the State Pension increase by last year?

Over the past 5 years, the New State Pension and Basic State Pension have increased by the following amounts under the triple lock (based on single-person rates only):

State Pension increases for the past 5 years

Will the triple lock return in the future?

Rumours of the triple lock being removed have been around for quite some time, but the pressure to scrap or amend the guarantee has accelerated since the coronavirus crisis started last March.

However, when the government announced they will be suspending it this year (for rises from next April), it was positioned as a suspension rather than a complete removal, with Work and Pensions Secretary Thérèse Coffey saying:

“We can and will apply the triple lock as usual from next year for the remainder of this Parliament, in line with our manifesto commitment.”

If you would like to learn more about pensions take a look at our pensions webpage or get in touch for a free initial chat about your own circumstances.

Please note this article offers information about financial planning and should not be taken as personal advice. Figures and data are correct at the time of publication.