Lifetime allowance (LTA) frozen for five years.

The standard lifetime allowance (LTA) will remain at £1,073,100 for at least the next five tax years (2021/22 to 2025/26). This freeze took effect from 6 April 2021 and breaks the current link between the LTA and the consumer price index (CPI). The government expects to raise around a billion pounds in extra tax revenue from this approach.

This article explores the impact of the LTA being frozen for five years and the key considerations for those who are close to breaching the LTA or who already have.

What is the lifetime allowance (LTA)?

The LTA is the maximum amount of tax relieved pension savings an individual can build up over their lifetime across all of their pensions (but excluding the State Pension).

Breaching the lifetime allowance incurs a tax charge on the excess.

The LTA is currently £1,073,100 (2021/22 tax year).

What has the LTA been in the past?

2020/21 - £1,073,100

2019/20 - £1,055,000

2018/19 - £1,030,000

2017/18 - £1,000,000

2016/17 - £1,000,000

2015/16 - £1,250,000

2014/15 - £1,250,000

2013/14 - £1,500,000

2012/13 - £1,500,000

2011/12 - £1,800,000

2010/11 - £1,800,000

2009/10 - £1,750,000

2008/09 - £1,650,000

2007/08 - £1,600,000

2006/07 - £1,500,000

What is the LTA tax charge and when does it apply?

Simply having pension savings worth more than the LTA does not trigger a lifetime allowance tax charge. Benefits are only tested against the LTA when a ‘benefit crystallisation’ event happens. There are a number of benefit crystallisation events, most typically when an individual takes money out of their pension or dies, and additional specific tests at age 75.

The LTA tax charge is 55% if the excess over the LTA is taken as a lump sum; and 25% if it is taken as an income.

Although it appears more attractive to take any excess as income, in addition to the LTA tax charge income tax is also payable on the income taken. This often results in a total equivalent tax charge of around 55%.

Is there any protection for the LTA?

Various forms of protection have been made available to protect against previous reductions in the LTA. Eligibility rules apply to each form of protection with some including the need to cease all future contributions or benefit accrual.

There are currently two forms of protection that can still be applied for – Fixed Protection 2016 (FP16) and Individual Protection (IP16).

Fixed Protection provides a fixed level of LTA based on the lifetime allowance available prior to a reduction, as such FP16 provides an LTA of £1.25m. The level of the LTA under Fixed Protection is irrespective of the value of the individual’s pension fund/benefits. Fixed Protection will be lost if further contributions are made, further benefit accrual occurs, or an enhanced transfer value is received after the relevant date.

Individual Protection gives individuals who think that the value of their pensions will be over the LTA when they come to take money out, a personalised LTA based on the value of their pension savings. IP16 allows someone whose pension fund/benefits are valued over £1 million to protect those rights, subject to an overall maximum of £1.25 million. This personalised LTA will not increase unless the lifetime allowance increases to a level greater than the individual's personalised lifetime allowance. In these circumstances the individual's personalised LTA would revert to the new standard lifetime allowance. A crucial difference from Fixed Protection is that an individual can still be an active member of a pension scheme.

There is currently no application deadline for FP16 or IP16.

There is no new form of protection associated with the change in April 2021 because the LTA is not reducing.

What is the impact of the LTA being frozen?

The immediate effect is that the expected rise in the LTA of around £5,800 due on 6 April 2021 did not happen.

When the freeze was announced by the Chancellor in the 2021 Spring Budget, it was stated that “95% of savers approaching retirement are unaffected” by the LTA. However, the LTA will now start to affect more people over time. This could lead some people with significant pension benefits to reduce their working time or retire earlier than originally planned. For example, it has been suggested that many doctors may choose to stop working for the NHS as a result.

This change also makes retirement planning more challenging, particularly for those close to the LTA. But it's important to remember that the LTA is not a ceiling on what can be saved into pensions.

There are many good reasons why those potentially affected should continue saving into their pension, especially if stopping funding means losing out on contributions from their employer.

What to consider if you’re close to or over the LTA.

As a starting point, someone in this position should only give up saving into their pension if there is a better alternative.

So if the net returns on pension savings (which could include employer contributions) are still greater than saving alternatives elsewhere, then an LTA charge may be a price worth paying.

The best course of action will depend on your individual circumstances and obtaining advice from specialists in this field is essential. Some important questions worth considering are:

Should you give up your employer pension contributions?

Does carrying on paying matching contributions make sense?

If your employer offers extra salary in exchange for pension contributions will you be better off?

Should you stop paying into your pension if this will lead to a tax charge on savings in excess of the LTA?

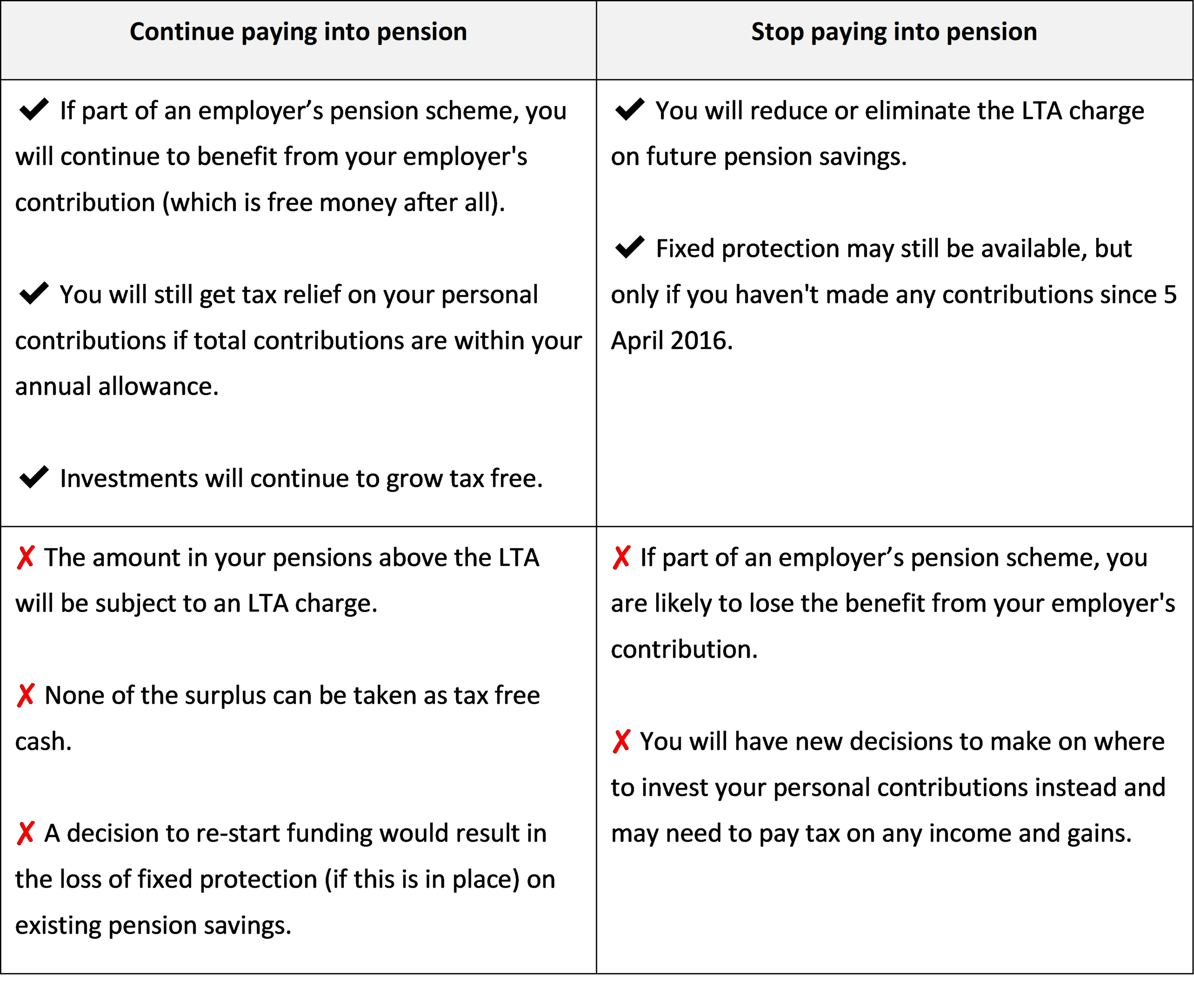

The pros and cons of continuing to pay into your pension

Making personal contributions that result in an LTA tax charge.

Funding above the LTA can make sense where it means retaining employer contributions. But what about making personal contributions which will result in an LTA charge? There's something that feels slightly uncomfortable about paying contributions knowing that an additional tax charge will be applied. What really matters though is what you will get back after all taxes have been deducted and the broader benefits and potential drawbacks have been assessed against your personal circumstances and objectives.

A key factor in the decision-making process is your likely tax position when you need to withdraw the money from your pensions. When considering investing in alternatives to your pension, other factors could also come in to play such as unused personal allowances, the starting rate band for savings and the personal savings allowance. Of course the availability of these will very much depend on individual circumstances.

This is why financial advice is so important.

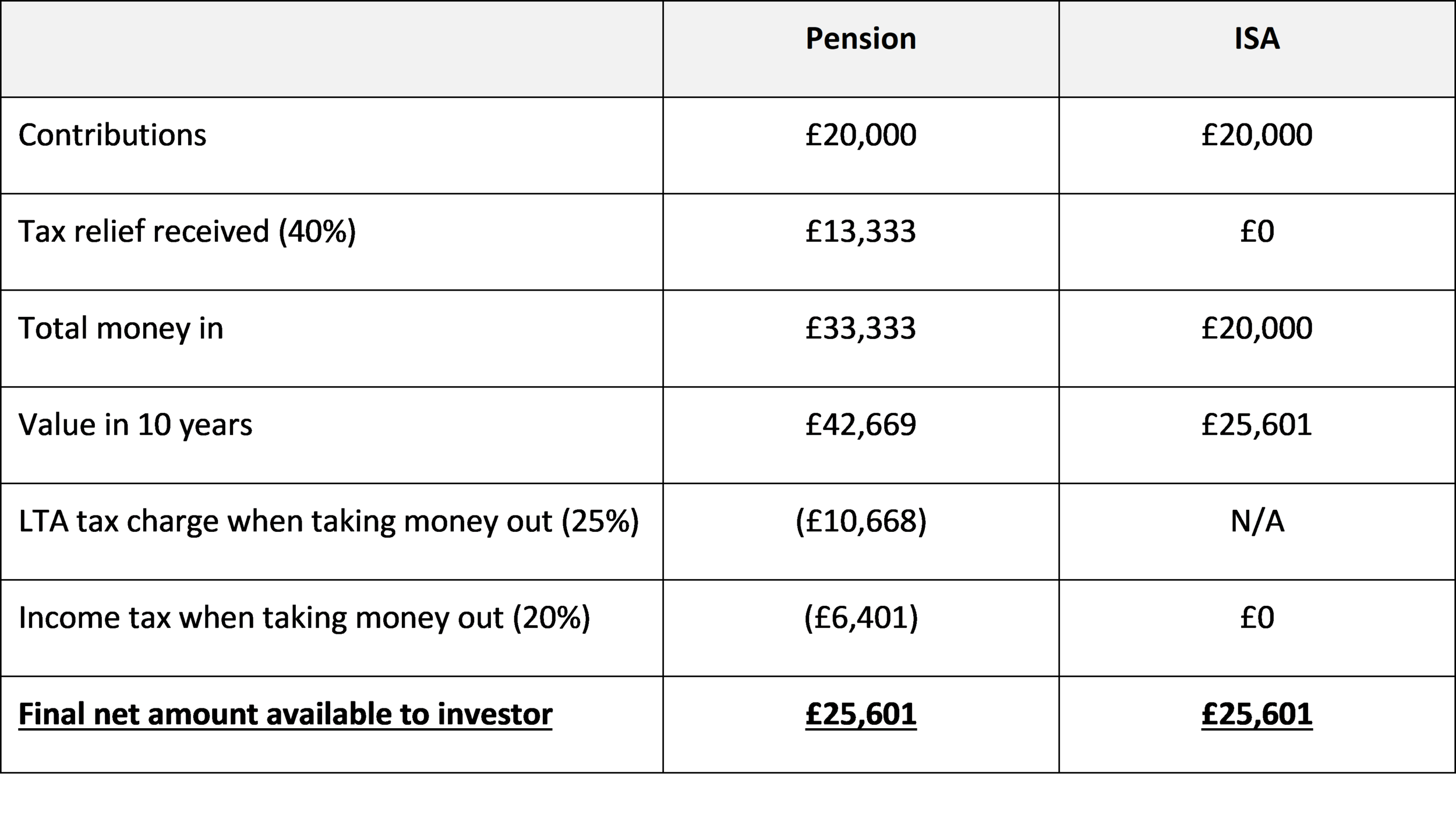

What about using ISAs instead?

Investment ISAs are generally considered the next best thing to pensions in terms of the tax advantages they enjoy. Although pensions benefit from tax relief on the money paid in and ISAs do not, both ISAs and pensions grow free of both capital gains tax (CGT) and income tax. ISAs have the additional benefit of being tax free when withdrawing the money. The only real downside for ISAs is that contributions are limited to £20,000 each year.

The table below compares what someone might get back from a personal pension and an investment ISA. It assumes the investor is a higher rate tax-payer when paying the money in, but a basic rate tax-payer when taking the money out. It also assumes a real rate of return of 2.5% over 10 years for the same net contribution of £20,000.

So in this scenario there is no difference between saving into a pension or an ISA. But if there are employer pension contributions available, then the pension will provide a much a better return. There may be more to consider if the pension income is taxed at higher rate, but even then this might be outweighed by the ‘free money’ from the employer contribution. An additional consideration would be if the excess over the LTA is less than 100% of the contribution paid in (as assumed above), in which case the LTA tax charge would be lower and the final net amount available from the pension would be higher.

But that's not the whole story. On death most pensions are free from Inheritance Tax (IHT), whereas ISAs will form part of the deceased’s estate and potentially be subject to tax at 40%.

Summary

It is natural to want to limit tax charges. But it's always important to look at the overall impact of any tax charges, in conjunction with the overall benefits on offer. Any possible alternatives to a pension will have their own tax consequences to be considered before reaching any conclusions.

If you would like help understanding your LTA position, whether a lifetime allowance charge may apply to your pensions, what course of action you should take in respect of your pension contributions, or applying for Fixed or Individual Protection please get in touch and one of our Chartered Financial Planners will be happy to help. An initial consultation is on us.

This article offers information about financial planning and should not be taken as personal advice. The value of pensions and investments can go up and down in value, so you could get back less than you put in. Any reference to legislation and tax is based on our understanding of UK law and HMRC practice at the date of production. These may be subject to change in the future. Tax rates and reliefs may be altered. The value of tax reliefs to the investor depends on their financial circumstances.