How have UK adults' investible assets changed over time?

How have UK adults' investible assets changed over time?

Introduction.

Since 2017, the Financial Conduct Authority's retail survey has monitored UK adults and their money. In this article, we look exclusively at their report on 'investible assets'. The report groups respondents into several bands, from no investible assets at all to more than £250,000.

Investible assets refers to an individual's liquid financial resources they could readily deploy or invest. In this context, they include cash savings held in bank or building society accounts, balances in current accounts and any funds in cash ISAs. However, it explicitly excludes longer-term or illiquid holdings such as defined-contribution pension pots, real-asset investments (for example, property or collectables) and any joint savings unless the respondent chooses to include their share.

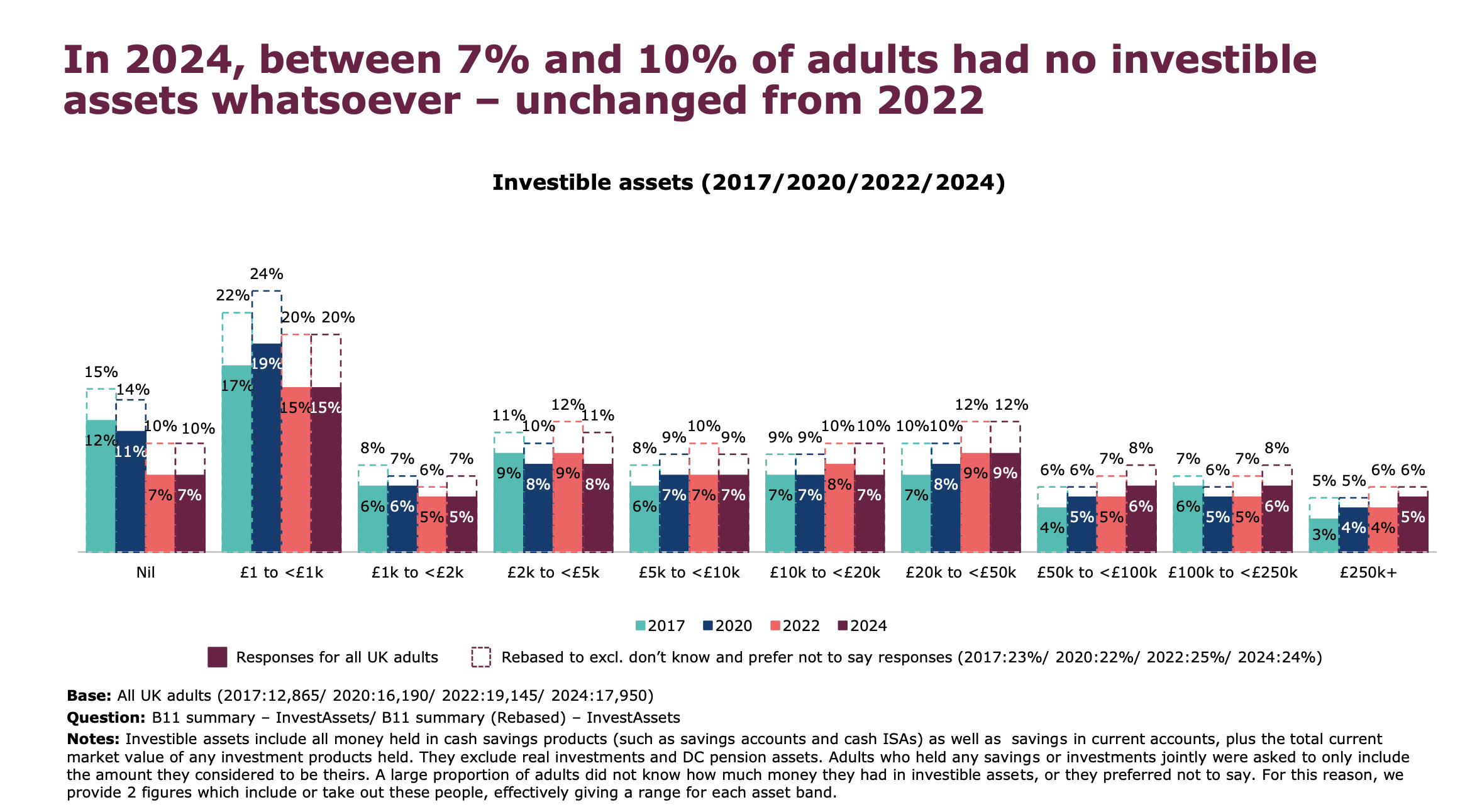

By rebasing the survey to omit "don't know" or "prefer not to say" answers, the reported percentages reflect only those adults willing and able to specify the amount they consider to be their investible assets.

Key findings from the latest report at a glance:

Zero-asset group remains flat.

There is a slight dip in the lowest positive bracket.

Mid-range bands edged higher.

Higher bands are rising slightly.

UK adults’ investible assets 2017-2024.

The zero-asset cohort.

Roughly one in ten adults hold no investible assets. That figure has barely budged since 2017, suggesting enduring barriers to saving. Low incomes, high living costs and unsecured debts are chief factors. Any strategy aimed at reducing zero-asset prevalence must tackle root causes, for example, improving access to affordable credit, raising financial literacy and ensuring wages keep pace with inflation.

Small savers.

Those holding £1,000 to under £5,000 account for around 27% of adults, down from 30% in 2017. Within that:

• The £1,000 to <£2,000 bracket slipped from 8% to 7%.

• The £2,000 to <£5,000 bracket stayed at roughly 11%.

These modest shifts suggest that some households are successfully building emergency buffers, a testament to the power of regular savings. By increasing regular micro-savings, such as automated weekly transfers, this cohort can take control of their financial future and potentially cross the next threshold, benefiting from compounding returns in a cash ISA or basic investment plan.

Progress for those with mid-range holdings.

The middle segments (£5,000 to <£20,000) grew by around one percentage point between 2017 and 2024:

• The £5,000 to <£10,000 bracket rose from 8% to 9%.

• The £10,000 to <£20,000 bracket held at 9–10%.

These figures indicate a steady trickle of savers advancing through the tiers. Once savers reach £5,000, they may want to start considering simple diversification or investments, such as low-cost funds in a Stocks & Shares ISA, alongside their cash.

Those with investible assets of £20,000 to under £50,000.

This cohort expanded from around 10 per cent in 2017 to approximately 12 per cent in 2024. Holders in this bracket typically have established cash buffers, often equivalent to three to six months' living expenses, alongside initial forays into equities or bond funds.

These savers routinely rebalance between cash, fixed income, and equities, ensuring they maintain sufficient liquidity while capturing market upside. Using their full annual ISA allowance can shelter gains from tax, and gradually introducing diversified global equity trackers or corporate bond ETFs will help them progress steadily into higher-value segments.

Finding this useful?

Once a month, we send our latest articles on pensions, investments, mortgages, protection, estate planning and more - along with a couple you might have missed. Practical reading for anyone taking their finances seriously.

Join our readers →Those with investible assets of £50,000 to under £100,000.

This segment grew from roughly 6 per cent in 2017 to about 7 per cent in 2024. Holders here typically combine substantial cash cushions with modest exposure to equities and corporate bonds. Individuals in this group will likely focus on refining their asset allocation, shifting a portion of cash into low-cost global equity trackers or investment-grade bond funds while maintaining a core emergency fund in easy-access accounts.

Those with investible assets of £100,000 to under £250,000

This group increased from around 3 per cent to 4 per cent over the period. These investors often benefit from both higher earnings and company share schemes. Their priorities include tax efficiency and risk management: making full use of annual ISA allowances, considering a lifetime ISA for children's education, and introducing a small allocation to their cash funds for diversification beyond public markets.

Those with investible assets of £250,000 and above.

Expanding from roughly 2 per cent to 3 per cent, this top tier represents a small but growing elite with multiple six-figure cash and near-cash holdings. At this level, bespoke strategies include structured products to smooth income, direct equity or bond holdings for greater control, and access to specialist vehicles such as property unit trusts or private equity partnerships. Rigorous annual portfolio reviews are essential to recalibrate exposure to higher-risk assets in line with their long-term objectives.

What are the drivers of change?

Several factors have influenced these trends:

Interest rates: Recent increases in interest rates from historic lows have eaten any spare income younger homeowners may have had to save, but they have benefited the older generations with little or no mortgage debt.

Cost of living: Dramatic increases in the cost of everything, in addition to the increase in wages, have put further pressure on those with limited savings ability.

Income inequality: An increasing wage gap means top earners have extended their saving advantage while lower earners struggle.

The rise in digital platforms and social media: The advent of more dynamic savings accounts and the availability of savings advice online are likely to have nudged more households into regular saving.

What are the policy and market implications?

The unchanged zero-asset share signals a need for targeted policy: matched-fund schemes or saver credits could incentivise those on very low incomes. Meanwhile, the industry could expand fee-free or micro-investment options to capture small balances. Enhanced financial education, particularly around budgeting and debt management, remains crucial.

What are the practical steps individuals can take to increase their savings?

Start with an emergency fund: Aim for at least £1,000 in a high-interest easy-access account.

Automate contributions: Even £10 or £20 per week builds traction over time.

Diversify beyond cash: Consider low-cost global trackers in a tax-free ISA once a £5,000 cash buffer is in place.

Review your allocation annually: Rebalance to keep your risk profile on track.

Conclusion.

From 2017 to 2024, the distribution of investible assets among UK adults has shown remarkable stability at the bottom and steady gains at the top. These patterns reflect wider economic pressures and evolving saving behaviours. For savers, the message is clear: small, consistent actions add up. For policymakers and advisers, the task is to lower barriers for those with none and to offer tailored guidance as assets grow. By combining disciplined saving habits with appropriate investment strategies, more adults can progress through each tier, ultimately strengthening household financial resilience.

What’s next?

Wherever you are in the UK, we invite you to book a free initial consultation with one of our experienced financial advisers. Whether you’re concerned about the economic outlook, managing your investments, planning for retirement, or better understanding pensions, we provide expert advice tailored to your needs. Based in Tunbridge Wells, Kent, we proudly serve clients nationwide.

Locally, we serve clients across Kent, including Ashford, Maidstone, Sevenoaks and Tonbridge. In East Sussex, we have clients in Bexhill, Crowborough, Eastbourne, Hastings, Heathfield and Uckfield.

Don't forget, this article offers general financial information and should not be taken as personal advice. Remember that investments and pensions can go up and down in value, so you could get back less than you put in. Tax rules can change and will depend on your individual circumstances.